GDP Growth

average growth rate by decade

This is the first edition of the United Kingdom Index of Systemic Trends. The UK Index is a dashboard on the performance and health of Britain’s political economy.

The UK Index seeks to assemble and provide the evidence in one place for a judgment as to the fundamental orientation and long-term direction of travel of Britain’s political economy as a whole – something largely absent from most of the present UK policy discussion.

It is intended as a corrective to overly narrow and short-term-oriented policy discussions in Westminster that continually miss the big picture of Britain’s longstanding decline by getting lost in the weeds of the latest policy relaunch, think tank report, or shallow political fad.

In addition, it offers a possible baseline and barometer by which can be judged the policy and political programmes of those who seek to offer easy answers – or, worse, the rebadging of past problems as future solutions – to the manifold structural social, economic, and political challenges facing Britain in the months, years, and decades ahead.

“All across the UK Index of Systemic Trends the dashboard warning lights are blinking fiercely, indicating the magnitude of the crisis that is unfolding – and will continue to unfold, unless there is a radical change in direction.”

The Democracy Collaborative first developed the Index of Systemic Trends for the United States of America, publishing a first edition of the U.S. Index in 2019 and a second edition in 2024.[1] With it, we have been able to predict with broad confidence the political and economic direction of the United States even in a time of extraordinary turmoil and chaotic change.[2] Taking the longer view helps reduce the noise and keeps the fundamentals in sight. In a time of crisis and flux, in which the recent past is no longer a reliable guide to the near future, the long-run trends are both clarifying and deeply unforgiving.

This looks likely to be just as true for Britain as it has been for America. As with the U.S. Index, our intention will be to revisit the data with a new edition of the UK Index every five years – a suitable time period after which to check back for substantial changes in direction.

Our findings in this first edition are stark but unsurprising.

All across the UK Index of Systemic Trends the dashboard warning lights are blinking fiercely, indicating the magnitude of the crisis that is unfolding – and will continue to unfold, unless there is a radical change in direction.

A political economy is a system, and the current system is organised to produce economic concentration, financial extraction, growing income and wealth inequality, and widening regional disparities.

This is even before we feel the full impact of ongoing and future shocks and disruptions such as climate change, artificial intelligence, and the increasing regionalisation of the global economy into competing (perhaps even warring) rival blocs.

By the measures included in this Index, the United Kingdom would seem to be woefully underprepared for the emerging challenges of the near future and lacking in even the most basic resilience. Moreover, none of these anticipated shocks are likely to lead to improvements in the case of the majority of the trends we examine, with most likely to accelerate the difficulties and make things still worse.

Taking the long view also brings the underlying dynamics of the system into focus. One of the signs that a crisis is systemic, rather than purely political or economic, is that key indicators decline or stay the same regardless of changes in political power or business cycles.

Since 1979, the United Kingdom has experienced six turnovers in the party-political composition of governments at Westminster. It has also experienced five recessions (and recoveries). Yet, as our Index demonstrates, on many important economic, social, and democratic indicators there has been little lasting improvement and, in many cases, substantial ongoing deterioration over the period as a whole .

Moreover, there is a clear suggestion that the crisis is accelerating. The numbers on collapsing public faith in democratic institutions are borne out by the tumult in the political system as one government after another is rapidly pitched into crisis.

Since 2010, Britain has had seven different prime ministers, compared to just eleven for the whole of the rest of the postwar era covering over half a century.

Six prime ministers in a single decade is not the sign of a functioning polity. In the absence of fundamental structural change, future governments will continue to be broken on the wheel of the crisis, in large part because they continue ineffectually to attempt to manage the existing model and are unwilling to reach for deeper, more systemic solutions.

“Since 1979, the United Kingdom has experienced six turnovers in the party-political composition of governments at Westminster [and] five recessions (and recoveries). Yet, as our Index demonstrates ... there has been little lasting improvement and, in many cases, substantial ongoing deterioration over the period as a whole.”

Overall, then, the picture offered here is rather a bleak one. However, the UK Index of Systemic Trends is not intended to be an elaborate exercise in doom-scrolling (although much that it contains is sobering and suggests cause for alarm). Nor would we wish to overclaim or exaggerate its importance: it is by no means a comprehensive or exhaustive study.

Rather, it offers a reliable snapshot as to the performance of Britain’s political economy as a whole over time.

It is therefore designed to be illustrative of what we believe is an extremely important insight: that the current UK political-economic system is consistently failing to deliver improvement across a variety of different measures; and that this is indicative of a systemic crisis – and of the need to move in the direction of a new system that can and will produce better outcomes.

We suggest some plausible basic elements of that new direction in the Conclusion.

The writing of this report has been a collective endeavour at TDC. The data was collected and analysed by Howard Reed of Landman Economics, a Democracy Collaborative fellow, for which we are truly grateful. The narrative was written by a team of Joe Guinan, Thomas M. Hanna, Neil McInroy, and Howard Reed.

Thanks to Joana Ramiro for organising us, to Matthew Brown, Martin O’Neill, and Ben Sellers for input, and to openbox9 for design and layout.

Joe Guinan

President

The Democracy Collaborative

Thomas M. Hanna

Vice-President of Research and Policy

The Democracy Collaborative

Neil Mclnroy

Global Lead for Community Wealth Building

The Democracy Collaborative

Howard Reed

Senior Fellow

The Democracy Collaborative

““I just do not accept that Britain is broken.””

Britain is broken – with the notable exception of the prime minister himself, this is now an uncontroversial claim, accepted widely across much of the political spectrum.

Everybody knows that all is not well in the United Kingdom – in the economy, in the regions, in communities – as is underscored by the profound and growing sense of anger and disquiet manifest in British politics and throughout democratic public life.

As we will show with the data that follows, Britain faces a systemic crisis.

At the heart of this systemic crisis is a political and economic model which – in its operations, functioning, and outcomes – is comprehensively failing to meet the needs of a growing majority of the population.

Ordinary people understand this, however much our policymakers and politicians seek to avoid the implications and run away from the consequences.

Work no longer pays, wages are not keeping pace with costs, while housing, education, and retirement are all growing increasingly unaffordable. Jobs have become unsatisfying, precarious, and insecure. Inflation in the price of essentials is resulting in a squeeze on living standards for all but the wealthiest.

The good life, for more and more households, is increasingly out of reach.

This lived experience of a fundamental shift is borne out by the economic data. Old assumptions that have long guided policymaking have been made obsolete by significant changes in the performance, operations, and outcomes of the UK economy.

All across the advanced industrial world growth has slowed, while the longstanding link between productivity and incomes has been severed. Technological innovation and increases in productive capacity no longer translate into prosperity for the many but rather place great riches in the hands of a tiny few. Income inequality continues to grow, while the overall concentration of wealth has reached obscene proportions.

This fact of an antisocial turn in the behaviour and functioning of the economy is leading to a comprehensive breakdown in the social contract.

This in turn lies behind the political turbulence of the last decade and a half since the Great Financial Crisis, which has seen seven (soon to be eight?) prime ministers in just fifteen years, almost as many as in the previous half century combined.

The continuing churn at the top is only the most prominent of the morbid symptoms of the current interregnum, to borrow words from Antonio Gramsci, whose widely quoted observation that “the old is dying and the new cannot be born” has become something of an epigraph for our times.[3]

This crisis poses existential challenges for a UK political class which, virtually alone among social segments outside of the donor class, retains a strong commitment to the present failing social and economic order. Increasing claims of “ungovernability” in the media are just a means of side-stepping the deeper meaning of the crisis now that the fact of the crisis has itself become unarguable.[4]

“A dangerous gulf remains between the magnitude of the systemic challenge and the inadequate scope and scale of the responses that are being conceived and proposed by the establishment political parties.”

The problem, however, is not some abstract “ungovernability” – a diagnosis which was also advanced in the 1970s, and which led to the installation of the current neoliberal economic model. Rather, it is that vested interests in the persistence of the status quo will not permit radical change of the order and depth that would be required to make the crisis manageable.

A dangerous gulf remains between the magnitude of the systemic challenge and the inadequate scope and scale of the responses that are being conceived and proposed by the establishment political parties.

The following data lay out the contours of this systemic crisis in Britain.

The economy is slowing, but even when there is growth it accrues to the top of the income and wealth distribution in a lopsided economic model that serves only the richest and leaves the rest behind.

For the last couple of decades, workers have been labouring through the longest period of wage stagnation since the Napoleonic wars.

Dominated by an outsized financial sector – the City of London – that has driven the long-term hollowing-out of UK manufacturing industry and the financialisation of the rest of the economy, the dominant experience for the majority of Britons has been the rise of “unaffordability.”

The term “cost-of-living crisis” has been applied with the insinuation that this is somehow a temporary aberration, linked to the pandemic and to the inflationary energy price shocks stemming from the Ukraine war and the US-Israeli attack on Iran, to be endured until normal economic service resumes.

Our Index suggests that this is not the case, and that the crisis is intrinsic to the economic model itself.

Britons have weathered the Great Financial Crisis, the COVID-19 pandemic, and now the costs of living crunch as part of what looks to be a major structural shift, a form of structural adjustment downwards of real wages and living standards that is occurring across the advanced industrial world but is taking a particularly acute form in the UK.

As the data will show, these outcomes are not accidental but are instead hardwired into the economy through patterns of ownership and financial flows, with a small elite of asset owners extracting increasing rents from the rest of us.

This is made possible both through the outsized role of the finance, insurance, and real estate (FIRE) sector in the UK economy, and because of the profound legacy of privatisation and concentration of wealth that was begun under Thatcher and Major, consolidated under Blair and Brown, further extended under the Coalition and the subsequent Conservative governments of Cameron, May, Johnson, Truss, and Sunak, and is again being left in place by Labour under Starmer and Reeves.

It is not fully appreciated just how extreme the legacy of privatisation is in Britain. HM Treasury calculated that, all told, between 1980 and 1996 Britain racked up fully 40 per cent of the total value of all assets privatised across the OECD.[5]

This is an astounding figure, denoting a massive transfer of wealth from public to private interests. Elsewhere, the only remotely comparable experiences occurred in countries – Pinochet’s Chile and the disintegrating Soviet Union – that were undergoing exceptional transitions and in which the rule of law was basically inoperative.[6]

Britain was leading the way in the creation of a new economic model by changing the economy’s underlying institutions and installing a neoliberal policy framework, shifting the balance of forces between public and private, and between labour and capital, decisively in favour of the latter.

This is one factor that has created today’s rip-off Britain.

The institutions and arrangements at the heart of today’s UK economy – concentrated private ownership, corporate dominance, the overweening might of London-based finance capital – together form one of the most powerful engines ever created for the extraction of wealth and its distribution upwards.

It is this basic design that drives the outcomes that can be seen in this Index in terms of crumbling public infrastructure, social atomisation, environmental degradation, widening regional disparities, stalled social mobility, and a widespread sense of popular disempowerment.

This is the picture of broken Britain that emerges clearly and unambiguously from the data below.

The trends considered in this UK Index of Systemic Trends include: growth, inflation, taxation and spending, poverty, income inequality, household incomes, wealth inequality, household wealth, wages, labour productivity, employment, unionisation, house prices, value of welfare benefits, public and private investment, output and employment by sector, financialisation and financial extraction, regional inequality, healthcare and NHS performance, maternal and infant mortality, life expectancy, domestic violence, suicide, incarceration, greenhouse gas emissions, and trust in government. It also investigates the cost-of-living crisis and the impacts of Brexit; and provides a cross-country comparison for certain economic and social indicators.

The trends are presented here with minimal analysis and argumentation, as a baseline in the reality of what is happening (and not happening) in the experience of most people in Britain.

Our intent is to make this material accessible in one place such that it lends itself to a long view and systemic horizon, setting the proper parameters on our understanding of what it will take to alter the course of many dangerous political-economic trends in the United Kingdom that have been decades in the making.

We hope that you find it useful.

That said, five stories stand out to us as worth highlighting from the mass of information contained below, and what it suggests politically and economically.

If Britain is broken, who broke it?

The first, and overarching, story that emerges from our survey of the UK political economy is the deep and fundamentally systemic nature of the current crisis and the huge gap between what the data shows and the stunning superficiality and inadequacy of most of what passes for political debate, policy discussion, think tank analysis, and media commentary in the country today.

This gulf is so large that it prompts us to reach for sociological and material explanations.

The detachment of the political class as a whole from the real issues and concerns of ordinary people throughout the country cannot be an accident, consistent as it is across Labour, Conservative, and Coalition governments.

It amounts to a reigning ‘Westminster Consensus’ in support of Britain’s failing economic model that must be dethroned before there can be any hope of substantive change and improved outcomes.

To have brought the British economy and society to this point of crisis and decline amounts to collective mismanagement by the political class as a whole, with the active collaboration of lobby journalists and legacy media.

In 1927, in a different period of malaise, the French writer Julian Benda published a controversial book called La Trahison des Clercs – in English, The Treason of the Intellectuals.[7] The book laid out the collective failure of the intelligentsia to perform their critical social function of dispassionate reason and detached analysis as they instead fell into line as the craven servants of power and ideology.

Given the evidence below, we have reached the point of needing to similarly call time on our own treasonous elites, and their co-optation, capture, and complicity in Britain’s perpetual state of decline, which now stretches out over half a century.

To look at the composition of Parliament, the media, the think tanks and nonprofits, and the establishment political parties is to see a mirror image of the advent of the new corporate and financial business class that has emerged in the UK – a power elite that has itself been “denationalized,” according to business scholar Stephen Wilks, in that it “is no longer committed to the British national interest or even to continued location in Britain.”[8]

This amounts to a class apart, with its own sectional interests in career advancement and material reward that leads to the enactment and preservation of a very different policy agenda than that which would be supported by a popular majority, if only they were offered an honest choice.

To concretise this treason of the UK elites, simply think of the average person in Hartlepool in 1992, the year that Peter Mandelson was first elected as their Member of Parliament, and look at the economic fortunes of that median individual over the intervening years as evidenced by the data in this Index – comparing it to how the system has delivered for Mandelson himself, and for his cronies.

In whose interests has the system really operated over that period? Ordinary people, or the politicians supposedly engaged in public service to represent them?

With the partial exception of the economic programmes that are being developed by the Greens, by Plaid Cymru, and potentially by Your Party, there is nothing on the table in policy terms today that is remotely capable of bending the curve on Britain’s long-term systemic crisis and decline.

Any insurgent political party presenting itself as anti-establishment or as a genuine break from the status quo of the Westminster Consensus should be asked to demonstrate concretely the ways in which they would depart from the current economic model that has been continuously failing the majority of people in the UK for decades.

Related to the treason of the elites and their misrepresentation of the people is the radical circumscription of the policy agenda and the misdirection of political and policy debates into areas that are irrelevant or largely beside the point.

The second story that leaps out from this Index is the extent to which our politics is organised around the pursuit of a chimera – the chimera of economic growth.

Almost the entirety of the economic policy agenda of the current Labour government under Starmer and Reeves is predicated on the elusive quest for growth – which has also been the stated goal of all the governments that preceded them in our period.

We are told that the state lacks sufficient resources to make the public investment that is obviously required, and that the government must therefore avoid frightening the horses with taxation or nationalisation and instead create the conditions business craves – deregulation, lower taxes, and fewer worker rights. This economic strategy, we are told, will encourage increased private sector investment and result in growth (“wealth creation”) that will benefit all.[9]

Everything about this approach is wrong – especially the backwards causal relationship between public investment and growth.

It would be difficult to discern from frontbench parliamentary discussions or the opinion and analysis pages of the national newspapers that growth in Britain – as our Index shows – has been consistently in decline, lower on average each decade than the decade before for the entirety of the period since the 1960s.

The only exception is the 2010s, which is explained by the recovery from the economic lows of the Great Financial Crisis in 2007-2009.[10]

But even in the 2010s, when considering GDP per capita, the average rate of growth was more than a full percentage point lower than that of the 1970s and 1980s (2.5% versus 1.3%).

There is absolutely nothing on the table in policy terms (and nothing external, in terms of global conditions) that suggests anything but a continuation of the dwindling of UK growth into the future.

Moreover, what feeble growth has occurred hardly suggests that additional growth would serve as a panacea.

When growth does occur in the present model, far from being broad based or trickling down it largely accrues to the top.

And some forms of growth, far from being beneficial, are actually its very opposite – the growth of the machinery of financial extraction and upwards redistribution.

The picture gets even worse with the third story evidenced by the data.

In a paper written for The Democracy Collaborative, the economists Dirk Bezemer, Michael Hudson, and Howard Reed have demonstrated that growth in the UK FIRE sector – “financialisation” – should be subtracted from rather than added to GDP, and growth in financialisation considered a growth in rent extraction.

Financialisation (to borrow their definition) is “the diversion of financial flows away from the real economy of production and consumption and towards asset markets in pursuit of capital gains.”[11]

“To have brought the British economy and society to this point of crisis and decline amounts to collective mismanagement by the political class as a whole, with the active collaboration of lobby journalists and legacy media.”

“There is absolutely nothing on the table in policy terms (and nothing external, in terms of global conditions) that suggests anything but a continuation of the dwindling of UK growth into the future. ”

“Financialisation is a complex phenomenon, but has enormous explanatory power as to the causes of Britain’s highly unequal and dysfunctional economy of growing poverty in the midst of great plenty. ”

Financialisation is a complex phenomenon, but has enormous explanatory power as to the causes of Britain’s highly unequal and dysfunctional economy of growing poverty in the midst of great plenty.

Far from boosting productivity and increasing efficiency in the non-financial economy, the growth of the financial sector functions as a subtraction from the real economy, as “financial flows are diverted to unproductive uses and… the resulting revenue flows benefit a minority. As financialisation gathers pace, rising wealth and debt detract from income for the majority.”

In such an economy, what is counted as growth matters a great deal. Every financial asset is at one and the same time someone else’s financial liability – and as the holdings of the financial sector have increased, so too has the debt held by households and businesses in the non-financial economy.

This process helps explain the squeeze-play of recent years, whereby nominal economic growth has in reality been experienced as reduced income through increased extraction and indebtedness.

The data for the UK economy show the powerful effects of financialisation.

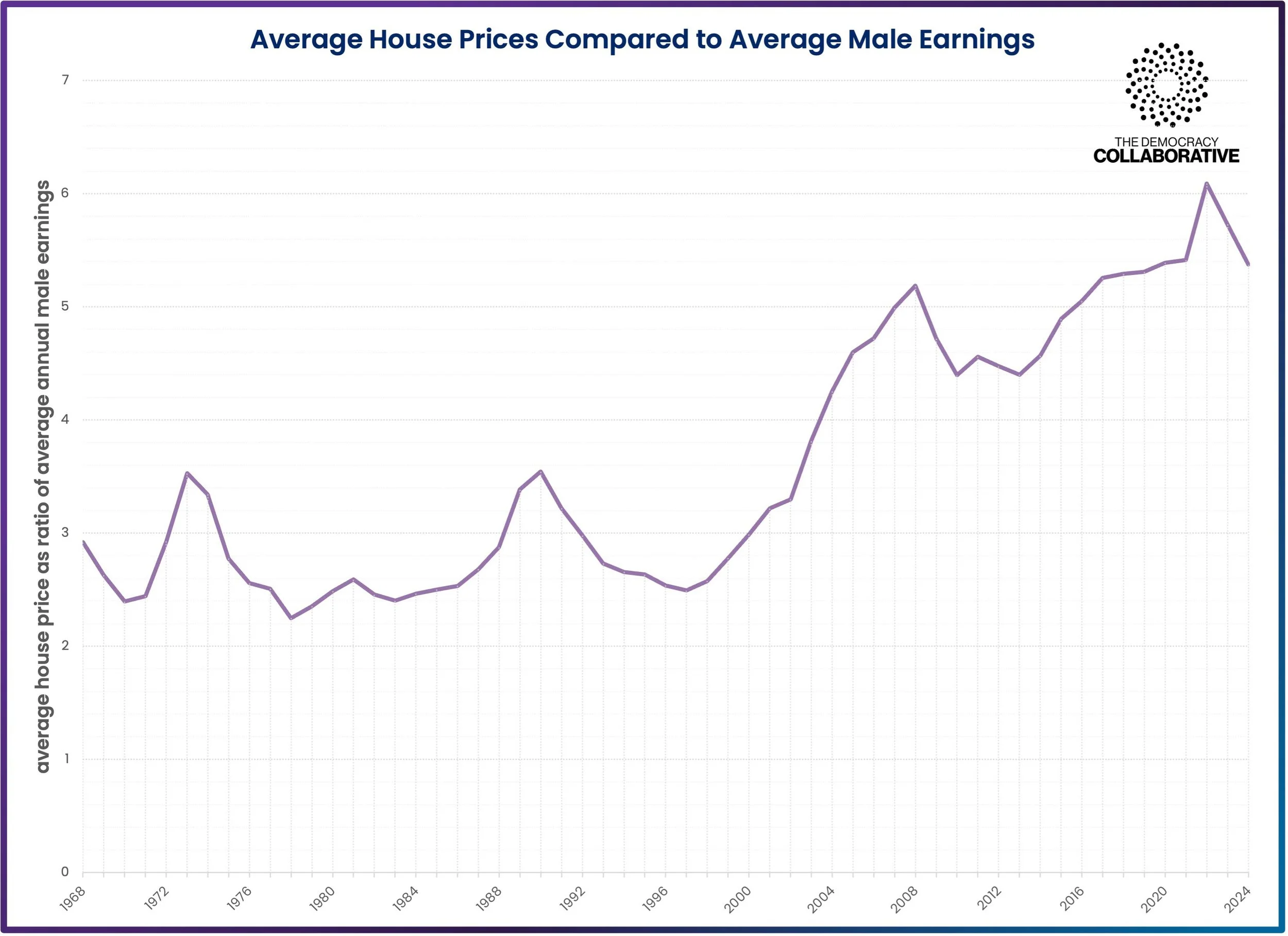

In the quarter century between 1995 and 2020, nominal wages doubled, nominal UK GDP rose two and a half times, average house prices quintupled, but the valuation of financial assets rose four and a half times.

The benefits of this “capital gains economy” flow primarily to the already wealthy, while for the rest of us there are lower earnings from work, lower income growth in the non-financial sector, lower productivity, and less innovation – all alongside sizable increases in debt and in financial and real estate wealth.

The City of London sits atop one of the most highly financialised economies in the world. It has long focused on finding new ways to extract “rent” from the rest of the economy rather than on productive investment or social need.

“The financial sector, then, is extractive from the real economy...and has also become the locus of the production of increased inequality in the UK economy.”

Richard Roberts and David Kynaston, who have written extensively on the history and practices of the City, even suggest that we think of it as “a foreign country” – but one whose activities have inordinately “big implications for government and industry” in Britain.[12]

As Guardian economics commentator Aditya Chakrabortty has said, commenting on London’s role as the world’s biggest offshore tax haven, “Britain either shrinks the City of London, or the City of London will swallow Britain.”[13]

The financial sector, then, is extractive from the real economy.

And given that all income groups are paying ever more into the finance sector in fees and interest charges and for underlying assets while the payouts from the sector are even more concentrated than those of the economy as a whole, the finance sector has also become the locus of the production of increased inequality in the UK economy.

This, then, is the economic engine that the current government (like its predecessors) has installed at the heart of its economics – a machine that lowers not increases growth, and concentrates the returns amongst the wealthiest asset owners, driving inequality and indebtedness.

The stated plan is to deploy this machine for financial extraction increasingly in public services, including the NHS, and in energy markets and infrastructure to supposedly drive the green transition. It will be a veritable bonanza for finance capital – and a very costly exercise for the rest of us.

Astonishingly, the government has effectively doubled down on one of the principal causes of Britain’s poor, uneven, and unequal economic development and rebadged it as the solution.

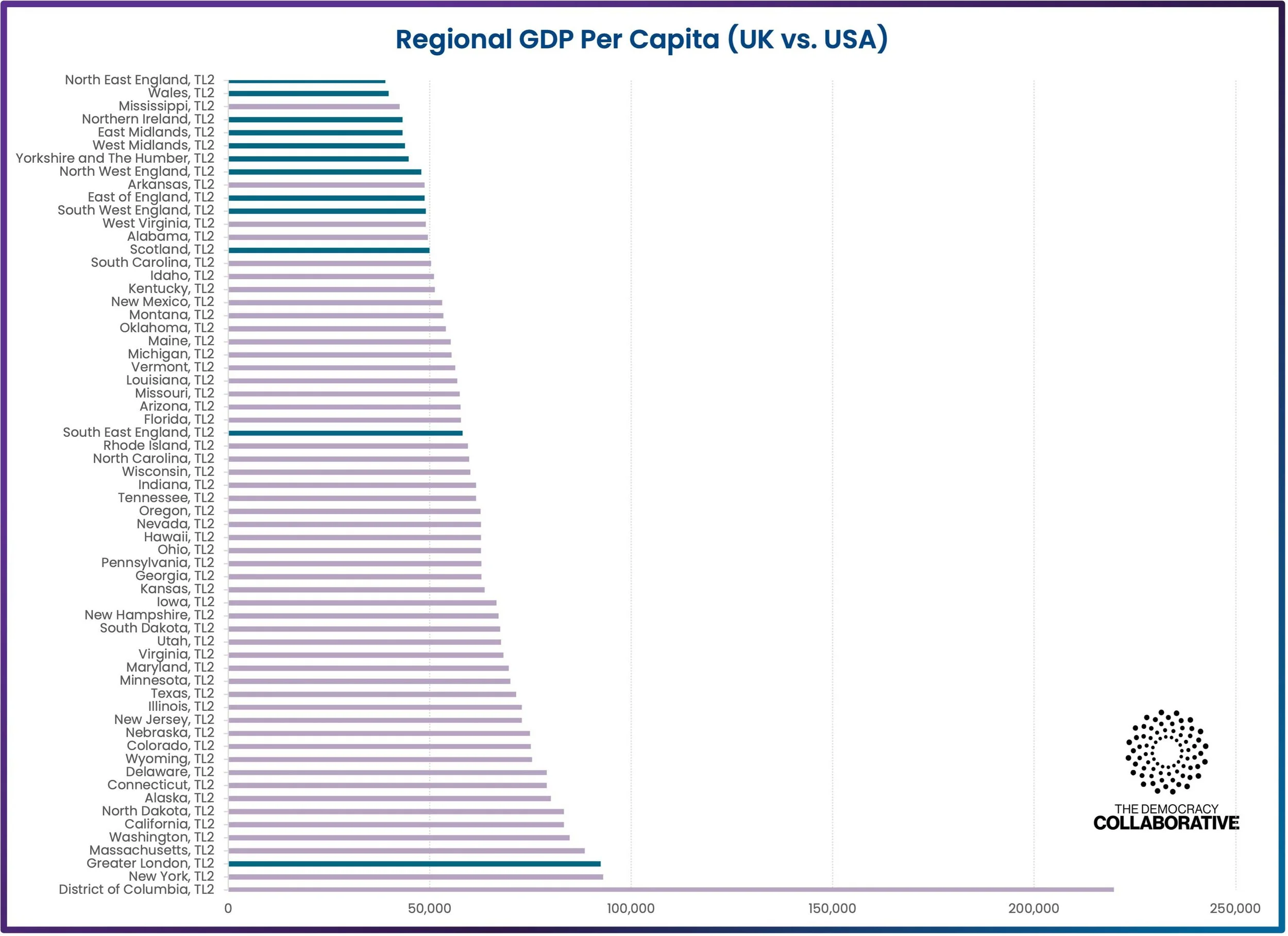

The UK’s yawning economic inequality is not just social but also spatial – Britain now has some of the deepest regional inequalities in the OECD.

The fourth story emerging from the data is therefore one regarding the regional worlds apart in which Britons increasingly live.

In the mid-nineteenth century, the Conservatives under Benjamin Disraeli fretted about the emergence of “Two Nations” in Britain – a wealthy upper class and an impoverished working class – and of the consequent implications for societal cohesion.

Today, the worry should be more along the lines of “Five or Six Nations.” Not only are Scotland, Wales, and Northern Ireland on very different trajectories to England, but England is itself made up of widely differing regions at increasingly disparate stages of development.

“Economic policymaking in Westminster clearly serves the economic interests of London and the South East, but is far from addressing the needs of not only the Celtic nations – which are on varying but distinct trajectories away from the metropolitan core of the British state, and thus away from the Union – but also of the English regions. ”

Regional GDP per capita offers a snapshot of this story. Looked at in constant 2020 prices and adjusted for purchasing power parity (PPP), the residents of different parts of the UK effectively live in the equivalents of vastly different countries at widely varying stages of economic development.

Somebody living in London, for example, is living in an economy the equivalent of Switzerland, whilst someone living in the South East of England is living in the equivalent of France.

Whereas people living at the other end of the regional scale are living in the equivalent of countries in Eastern Europe or the Baltic states: the closest comparison by Gross Value Added (GVA) for the North East of England is the Slovak Republic; for Yorkshire and the Humber, and the West Midlands, it’s Lithuania; while for the East Midlands it’s Poland, and for the South West it’s New Zealand.

Scotland, meanwhile, is closer to South Korea; Northern Ireland to Spain; and Wales to Hungary.

There is no longer a common story or unified direction for the countries and regions of the UK, many of which are now facing entirely different economic circumstances from those at the metropolitan core.

As a result, it no longer makes sense to talk in terms of a United Kingdom so much as a Disunited Kingdom, in which the state is no longer cohesive or coherent.

Economic policymaking in Westminster clearly serves the economic interests of London and the South East, but is far from addressing the needs of not only the Celtic nations – which are on varying but distinct trajectories away from the metropolitan core of the British state, and thus away from the Union – but also of the English regions.

Regional disparities alone, however, do not represent a cohesive alternative viewpoint, as there are also vast differences and inequalities within regions.

Greater London contains economic inequality gaps as big as those of the UK as a whole. Someone living in Camden, or the City of London, or Westminster, for example, lives in a borough with a level of development comparable to Luxembourg, while for Haringey or Islington it’s Switzerland.

In Kensington and Chelsea, and in Hammersmith and Fulham, it’s Ireland. For Lewisham and Southwark, and for Lambeth, the comparator would be Norway.

At the other end of the scale, residents of Enfield and Bromley live in the equivalent of Portugal; while those in Ealing live in Estonia; those in Croydon, in Slovenia; and residents of Barking and Dagenham, and Havering, live in an economy with a stage of development equivalent to Latvia.

In Redbridge and Waltham Forest, the comparator would be Chile.

It is clear from this Index that Britain is entering what will almost certainly be a period of great international instability and challenge in a condition of precarious fragility and extraordinary exposure to systemic shocks, both internal and external.

Decades of neoliberalism of different varieties has hollowed out and denuded the UK state of governing capacity and its people of resilience.

The tremendous shock sent through global energy markets by the US-Israeli attack on Iran in early 2026 highlighted Britain’s extraordinary exposure to international events. More than most, the country was caught on the hop by the energy crisis stemming from the war, which quickly threatened to spread out from maritime and shipping to finance, commodities trading, insurance, transport, petrochemicals, fertilizer and food production, medicine, manufacturing, and more.

The overextended supply chains and just-in-time production models of peak neoliberal globalisation are ill-suited to today’s emerging new world order (or disorder), characterised by wars, pandemics, and trade and financial instability. “What appears at first as a maritime blockade,” as one observer put it, “is in fact the exposure of the entire global system as a hierarchy of brittle interdependencies.”[14]

As a highly internationalised economy with a longstanding trade deficit in goods and low buffer stocks of both energy and food, the UK is particularly exposed to global shifts and especially to sudden shocks like the Persian Gulf energy crisis. As a result, upon the outbreak of war the International Monetary Fund immediately downgraded UK growth forecasts, already low, more sharply than for any other G7 economy.[15]

The fact that Britain is so far from self-sufficient in food and energy, and has eroded so much domestic manufacturing capability, leaves the UK as a sitting duck in the face of the growing storms ahead. The current UK debate on national security quickly falls into typical ‘Westminster Consensus’ thinking about military expenditures and readiness for war. But predictable calls to boost military spending are entirely beside the point in a country that increasingly lacks the ability to produce for itself through a strong manufacturing base.

In most other advanced economies, the preservation of such basics as virgin steel production capacity would be considered an issue of vital national security, falling within the scope of measures such as the Defense Production Act in the United States or resulting in emergency nationalisation of a kind regularly employed by France (where even the ownership of a large yogurt company was considered a matter of strategic national importance).[16]

In fact, the lack of an industrial strategy worthy of the name is a far greater threat to UK national security than the supposed failure to meet artificial targets for increased ‘defence’ expenditure on American-made armaments that will themselves only add to risk and dependency.

One of the factors in the creation of the original early twentieth century government programmes that were precursors to the creation of the postwar welfare state – the Education (Provision of Meals) Act, the introduction of medical inspections in schools, the Old Age Pensions and National Insurance Acts – was the discovery of the dire overall condition of the nation in terms of public health, fitness, education and skills, “national efficiency,” and general lack of preparedness in the face of brewing international storms.

Economic and social lack of preparedness are likely to prove far more serious weaknesses than neglect of a costly but impractical military posture in an era of non-traditional threats and risk profiles and asymmetric warfare.

It’s easy to become alarmist about the fragility of globalisation and over-extended international supply chains and just-in-time production with no redundancy or elasticity, leaving us on current stocks and without resupply and with the potential onset of energy outages just mere days from food riots in major cities. Thankfully, such nightmare scenarios have not yet transpired.

But today we can say with high degree of certainty that the UK is in no condition to meet the emerging challenges of the dangerous future world that is shaping up, whether in terms of neo-mercantilism and competing regional blocs, the scramble for natural resources, or the many and pronounced downstream effects of climate and other shocks to interconnected global systems such as food, energy, trade and investment.

Broken Britain, as evidenced by the data in this Index, is not beyond repair. It is, however, beyond the reach of ameliorative reform or tweaks around the edges to the dominant economic model. What it requires is deep systemic change.[17]

“We need a political conversation in Britain that goes beyond the limits of establishment policy positions and tinkering around the edges to the core issue of economic system change itself. ”

One key overall lesson from this Index is the relative fragility and insufficiency of after-the-fact policy “fixes” – whether in terms of tax-and-spend redistribution, or regulatory interventions, or both – as any kind of substitute for deep structural interventions in the core institutions and relationships of the political economy.

We need a political conversation in Britain that goes beyond the limits of establishment policy positions and tinkering around the edges to the core issue of economic system change itself.

If we are not to find exactly the same pattern of results and outcomes another five years down the line, then there will need to be an altogether different and more ambitious set of interventions in the years ahead, commensurate with the scale of the challenge and capable of setting the United Kingdom on a very different trajectory from our present, downward one.

This will require nothing short of a transformation in the ownership and control of the British economy and whose interests it is designed to serve.

The data in the UK Index of Systemic Trends is drawn from a variety of government and NGO databases. In all cases, efforts were made to obtain the most up-to-date information. However, in some cases (especially for the country comparisons) the latest available data may be from different years.

In most cases we have retained the definitions and terminology from the original data sources – including, most importantly, the use of “United Kingdom.” That is an artefact of the organisation of the data, and should not be read as support for the current constitutional positions of Scotland, Wales, or Northern Ireland.

Unless specified otherwise, UK data charts in this Index which display monetary values (such as average household incomes, average individual earnings and productivity measured as output per worker or output per hour worker) are uprated to the latest year in each chart using price deflators. Three different indices are used:

For statistics relating to household incomes (such as incomes, earnings and the value of welfare benefits) where the time series begins in 1988 or later, the Consumer Price Index (CPI) is used.

For income-related statistics where the time series begins before 1988, the Retail Price Index (RPI) is used.

For productivity, the GDP deflator is used.

For most of the period covered here (up until 2010) the RPI served as the UK’s primary measure of inflation. From 2010 onwards, however, the CPI became the official benchmark, aligning the UK more closely with international standards, particularly those used in the US and across Europe. Despite this shift, RPI continues to be published and remains relevant for certain contracts and historical comparisons. The UK Office for National Statistics only publishes detailed CPI data back to 1988 (although an imputed summary CPI measure is available back to 1955). Therefore, we have chosen to use the RPI for longer-run time series charts in this Index publication, with CPI used for short-run charts.

Inflation using the RPI measure is slightly higher in most years than the CPI or the alternative CPI(H) measure (a version of the CPI which includes housing costs in the index).

In 2016, Britain voted in a referendum to leave the European Union. After years of negotiations led by the Conservative government, this became effective in January 2020. The relatively haphazard and ideologically motivated departure from one of the world’s largest political and economic unions has undoubtedly had a significant effect on Britain’s economy, society, and politics. For instance, recent modelling by Bloom, et al. (2025) suggests that Brexit reduced Britain’s GDP by 6-8%, investment by 12-18%, employment by 3-4%, and productivity by 3-4%.[18]

While these effects are undoubtedly significant, this Index demonstrates that many underlying economic and social trends were in decline or stagnating well before 2020. While Brexit may have accelerated or exacerbated some of these trends, in most cases it was not the original cause.

Britain is in deep long-term economic difficulties.

We can see this when we look at the standard indicators used to measure economic health. The overall picture is one of stagnation, inequality, stark and growing regional disparities, and widespread social decay.

“The British people have been widely let down by the economic model that was installed in the 1980s, and by the political leadership that continues to hold in place and maintain a failing model through persistence with outdated and damaging public policies.”

The British people have been widely let down by the economic model that was installed in the 1980s, and by the political leadership that continues to hold in place and maintain a failing model through persistence with outdated and damaging public policies – something that has been true no matter what the party composition of the government of the day.

It is important to emphasize that this is true not only when viewed through the lens of alternative progressive frames of reference such as Wellbeing or the Human Development Index but also when the performance of Britain’s economy is looked at through the orthodox measurements by which the system prefers to measure itself.

The health of an economy is usually evaluated using a set of conventional measures of economic performance that include growth, employment, productivity, wages and incomes, inflation, and poverty.

A degree of caution is required in the use of such measures.

As the gap widens between headline economic numbers and how ordinary people are experiencing the economy in their everyday lives, conventional indicators are increasingly recognized as inadequate and insufficient, leaving out many important measures of societal health and wellbeing. Many of them were in fact never intended for the widespread policy uses to which they have continually been put.

In National Income 1929-32, the first calculation of what became gross domestic product (GDP), the authors (including Simon Kuznets) cautioned that “the welfare of a nation can, therefore, scarcely be inferred from a measurement of national income as defined above.”[19]

Among the famous limitations of the calculation of GDP are that only products or services transacted in the market are included, whereas factors such as household production, volunteer work, income from barter, and subsistence work are excluded.

Moreover, market prices determine the contribution of a product or service to the total, regardless of any consideration of social value. Every pound spent on tobacco and alcohol, bombs, or oil spill clean-ups provides the same contribution to GDP as a pound spent on education, food, or housing, when there is clearly a vast difference in their social value.

The value of natural and man-made assets available to an economy and society are also not considered in GDP. When a country clear-cuts a forest, the value of the resulting timber is counted as a positive contribution, while the loss of the forest itself (and all the ecosystem services it provides) is absent from the accounting.

Nor does GDP include any information on social equity: it is silent on income distribution, poverty, and much else besides. GDP also does not include any information on non-economic factors that affect collective and individual quality of life, such as health, freedom, physical and financial security, and political empowerment.[20]

There is also a deep academic and policy literature on both the ecological and social limits to growth, dating back to the 1970s.[21]

“In particular, they demonstrate that the economic model that has remained dominant in Britain (as elsewhere) over the past several decades is comprehensively failing – even when looked at on its own terms and using its own preferred measurements.”

For all these reasons, we should be sceptical of the value of the conventional set of purely economic measures as a definitive gauge of societal health and wellbeing. That said, these measures remain useful as indicators of some of the long-run trends as to how well an economy is functioning overall (and for whom), and thus remain important to consider.

In particular, they demonstrate that the economic model that has remained dominant in Britain (as elsewhere) over the past several decades is comprehensively failing – even when looked at on its own terms and using its own preferred measurements.

When looked at using these common economic indicators, Britain’s economy is mired in serious long-term difficulties.

Chief among conventional economic indicators is growth – and specifically growth in GDP.

In Britain, as in many countries, GDP growth has become both a catchall indicator of how the economy is performing, and the holy grail of economic policymaking for governments of all party political stripes to pursue.

Prior to winning the July 2024 UK general election, the Labour Party under Keir Starmer set out a target of 2.5% annual GDP growth, aiming to produce the highest per capita growth in the G7.

There is little reason, based on the long-run growth data on the British economy and the limitations of the kinds of measures contemplated in current UK policy frameworks, to think that such a target is anywhere near realistic or achievable.

In fact, the data suggest the opposite – that, absent major structural interventions or a radical change in the direction of economic policymaking, the UK’s elusive quest for growth is likely to prove the continuing unsuccessful pursuit of a chimera.

Britain has experienced a clear and significant decline in economic growth since the 1970s. During that decade, as well as the 1980s, average annualized GDP growth per capita was around 2.5%. In the 1990s it fell to around 1.8% and in the 2000s it was just 1.1%. The 2010s saw a slight uptick to 1.3%, primarily due to the recovery from the 2007-2009 Great Financial Crisis in the early years of that decade, but still well below averages from the 1950s through the 1980s. From 2015 to 2024, average growth was just 0.8% per capita.

Relying upon increased economic growth for improved economic and social outcomes, on Britain’s current trajectory, is a policy illusion – a persistence of the fallacy of “trickle-down” neoliberal economics, for all the disclaimers from politicians to the contrary. Half a century of experience points in the other direction. With the exception of the 2010s, Britain’s economic growth has been lower than the preceding decade for every decade since the 1970s.

Chart 1: GDP Growth

Source:

Office for National Statistics. Gross Domestic Product: Chained Volume Measures, Seasonally Adjusted (£m). Series ID: ABMI. Accessed 26 December 2025. Available at: https://www.ons.gov.uk/economy/grossdomesticproductgdp/timeseries/abmi/ukea.

Office for National Statistics. Estimates of the population for the UK, England, Wales, Scotland and Northern Ireland. Published 26 September 2025. Available at: https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/datasets/populationestimatesforukenglandandwalesscotlandandnorthernireland.

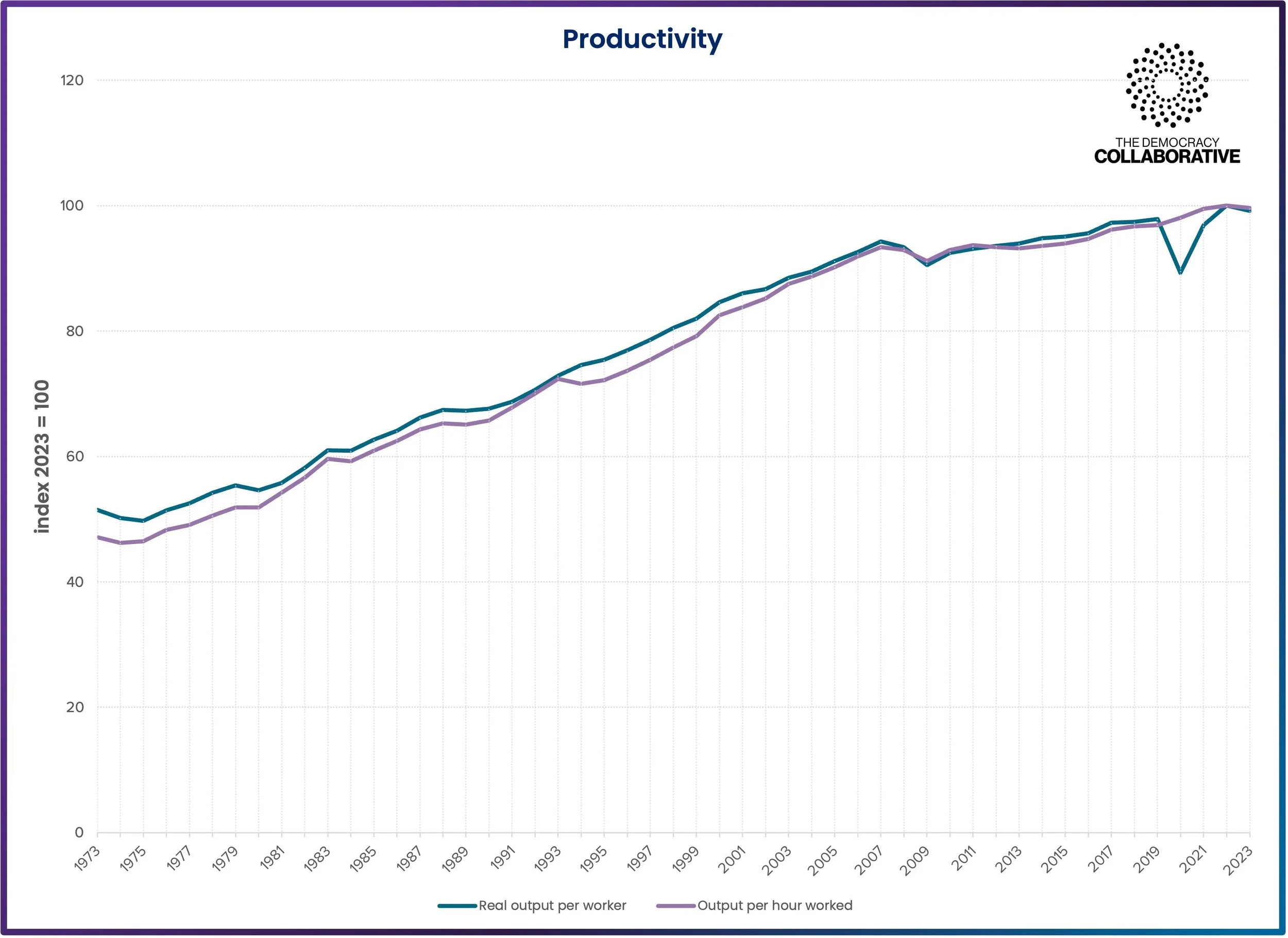

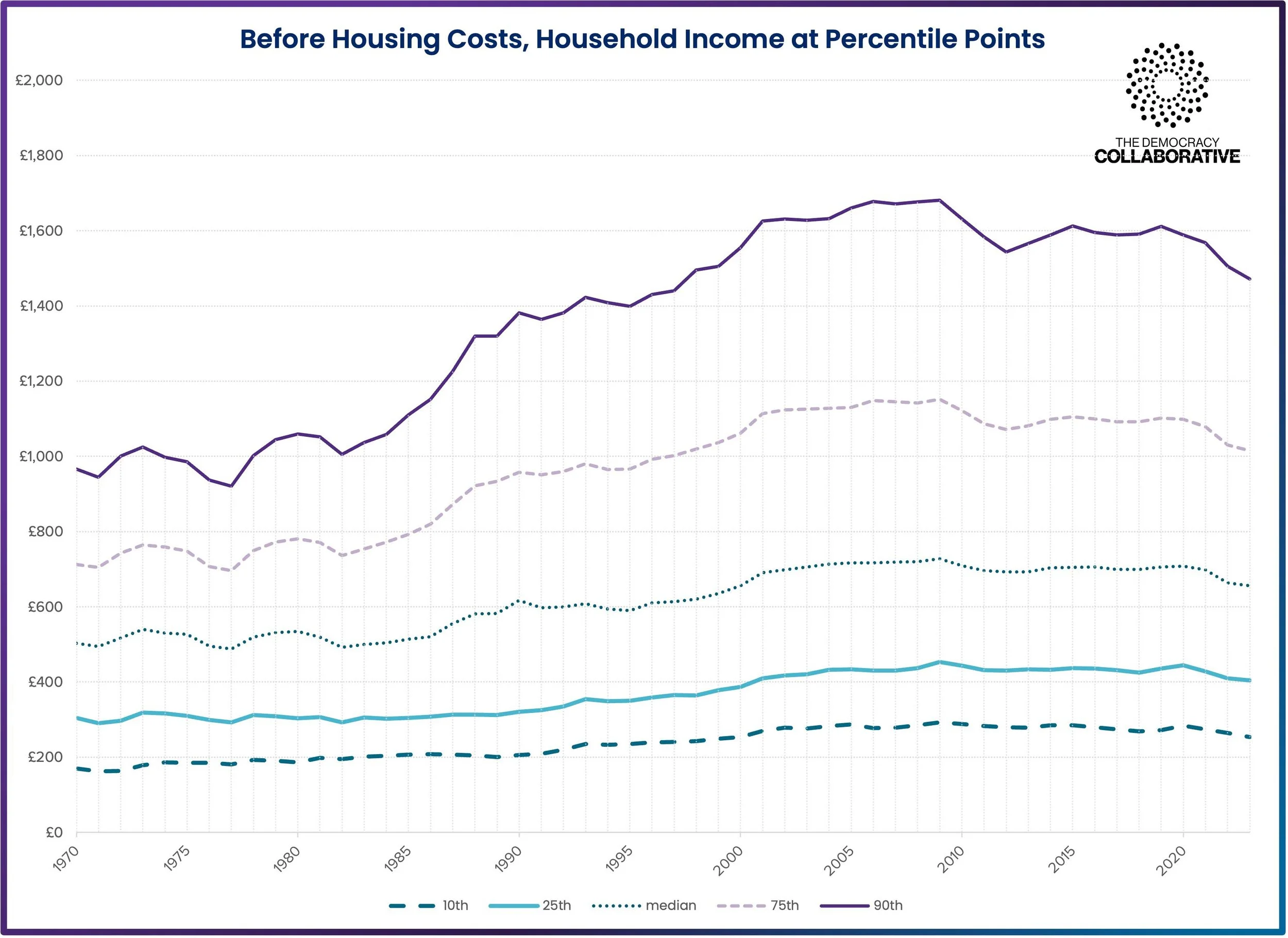

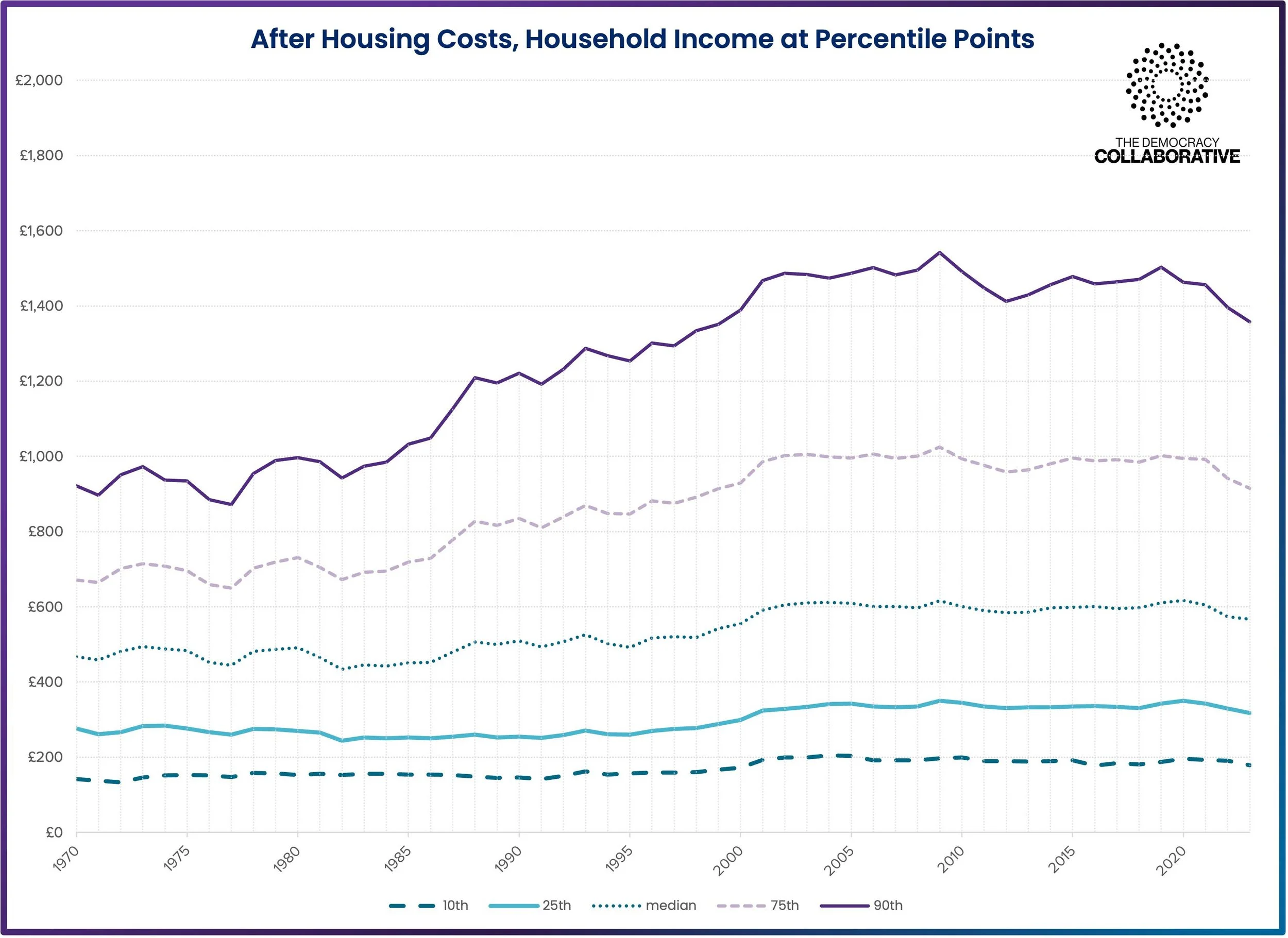

In 1973, mean real weekly household income BHC (before housing costs) was around £591.[22] By 2023, this had risen to around £818 – a 38% rise in 50 years (and an average of 0.4% a year). At the same time, real output per worker before housing costs (i.e. productivity) increased 92% over this period, an average of 1.6% per year.

In other words, over the last 50 years incomes have not kept pace with worker productivity. Even as the productivity of workers and the economy increases, workers no longer receive an equivalent increase in their pay packets. As is also the case in the United States, most of the gains from increased productivity are not passed on to workers in Britain but instead accrue to the top, to asset holders and the owners of capital.

Furthermore, incomes have stagnated since the dawn of the twenty-first century. In 2000, mean real weekly household income (before housing costs) was £849. In 2023, it was down to £817 (a drop of 3.7%). Real wages have not improved over where they were at the turn of the millennium – in other words, most workers have not received a real-terms pay increase in a quarter of a century, the longest period of wage stagnation since the Napoleonic Wars.

At the same time, productivity has continued to increase, rising by 17.25%. This suggests an accelerated decoupling of income and productivity in recent decades. Under any continuation of current economic arrangements, future increases in productivity in the UK economy will most likely not for the most part accrue to wages.

Chart 2: Income (Before Housing Costs)

Source:

UK Data Service. Family Expenditure Survey (1961–1993) and Family Resources Survey (1994/95–2023/24). Analysis by Howard Reed.

Source:

Office for National Statistics. Labour productivity time series. Published 13 November 2025. Available at: https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/labourproductivity/datasets/labourproductivity.

Source:

UK Data Service. Family Expenditure Survey (1961–1993) and Family Resources Survey (1994/95–2023/24). Analysis by Howard Reed.

Source:

UK Data Service. Family Expenditure Survey (1961–1993) and Family Resources Survey (1994/95–2023/24). Analysis by Howard Reed.

Poverty in Britain fell considerably after the Second World War – due, at least in part, to transfer policies and a major governmental focus on improving economic and social welfare through the creation of the postwar welfare state.[23]

For a time, significant progress was made in tackling the “Five Giants” of the famous Beveridge Report: want, ignorance, disease, idleness, and squalor. Absolute destitution was significantly reduced in this period.

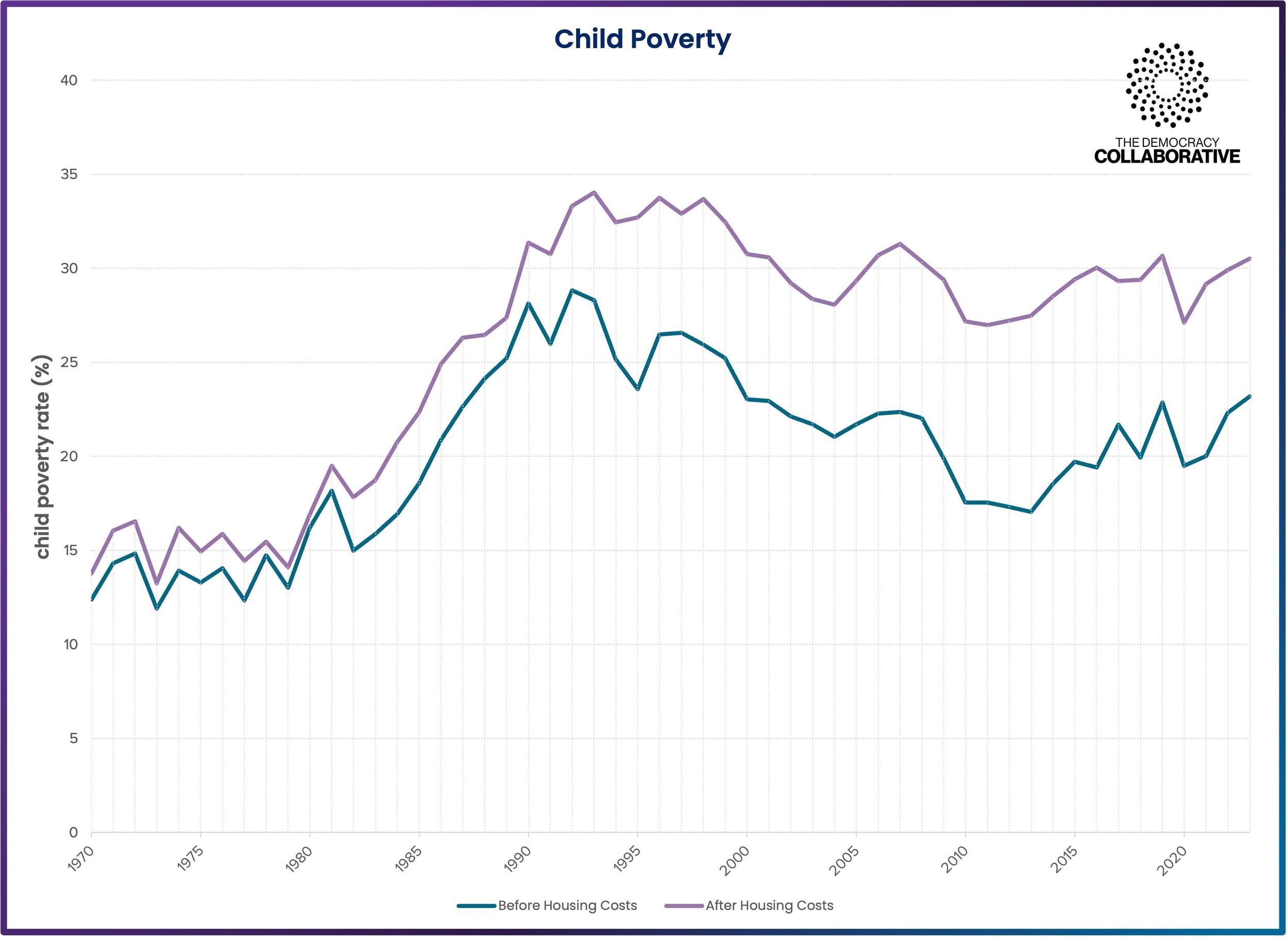

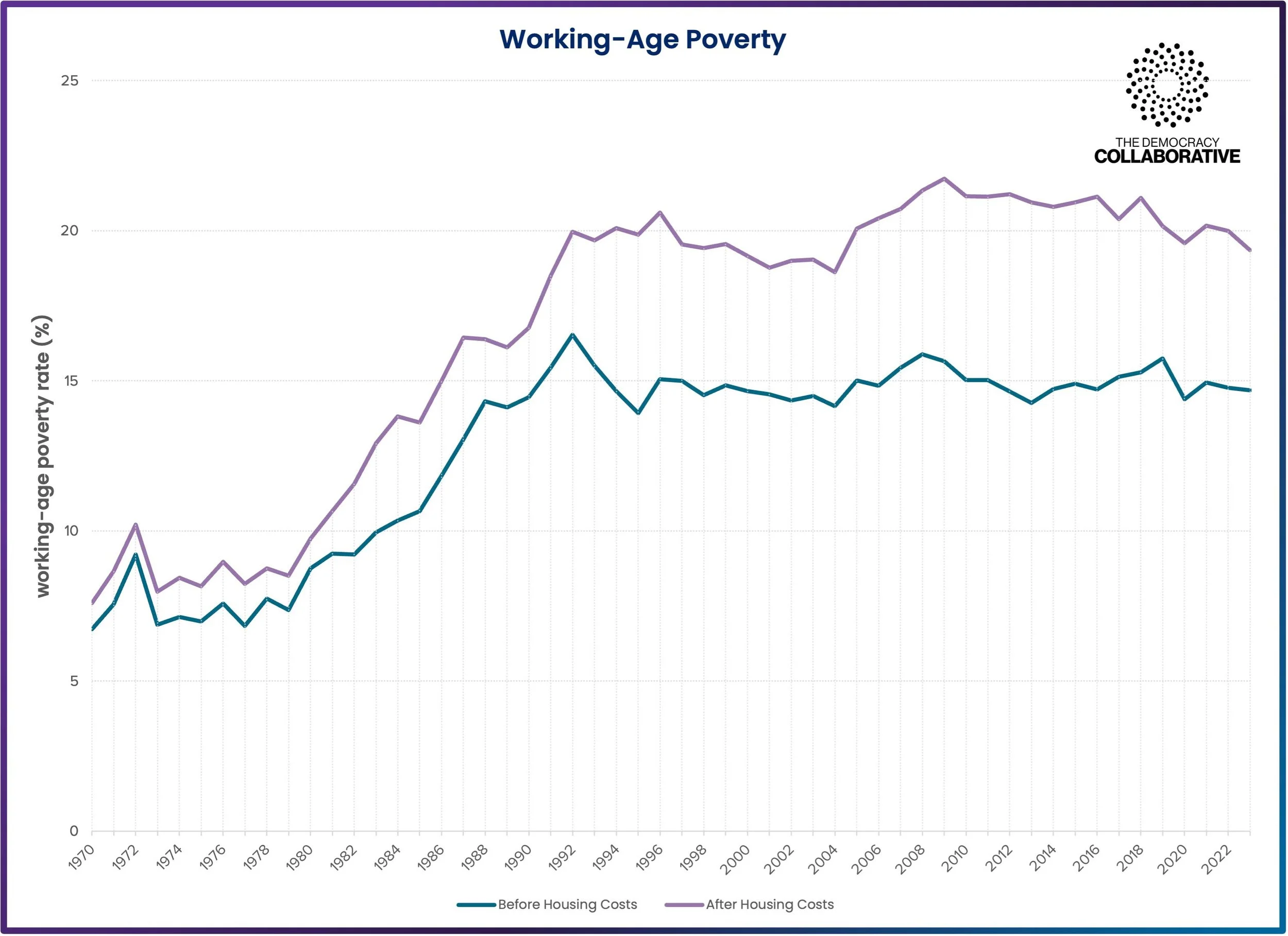

By 1970, the percentage of all Britons living in relative poverty (after housing costs) was down to 13.8%.[24] For children it was 13.7%, and for working-age adults it was 7.6%.

Starting in the late 1970s, poverty rates began to spike considerably and have remained at elevated levels ever since. In 2023, 21.1% of all Britons lived in poverty (a 52.9% increase from 1970). For children, the rate was 30.5% (a 122.6% increase) and for working-age adults it was 19.3% (a 153.9% increase).

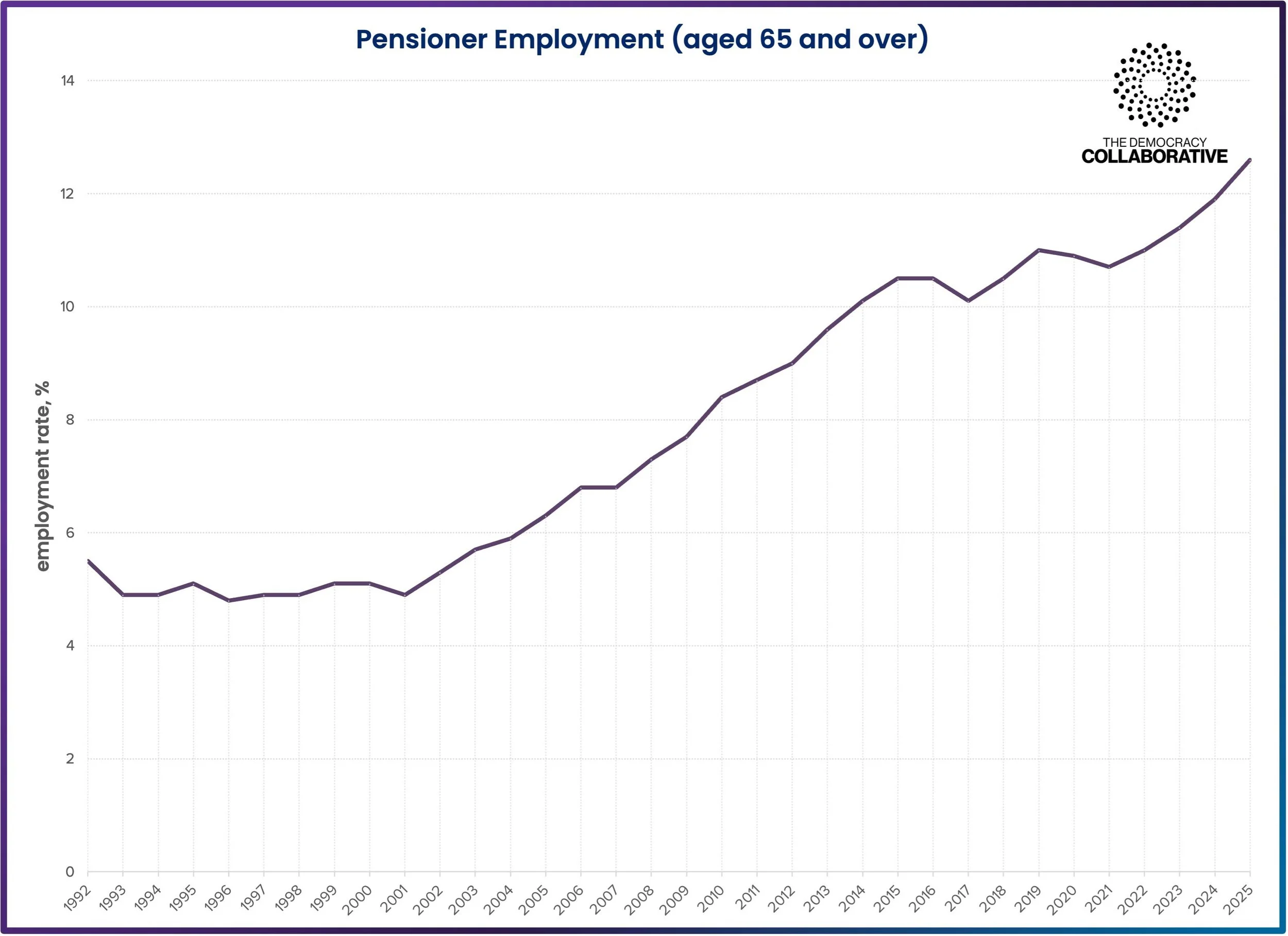

One area that has seen some improvement since the 1970s concerns the number of pensioners living in poverty (a drop of 58.4%). However, this may be at least partially attributable to a large increase in the number of pensioners having (or choosing) to work past the official retirement age.

Chart 6: Poverty Rate, All Households

Source:

Institute for Fiscal Studies. Living standards, poverty and inequality in the UK. Available at: https://ifs.org.uk/living-standards-poverty-and-inequality-uk.

Source:

Institute for Fiscal Studies. Living standards, poverty and inequality in the UK. Available at: https://ifs.org.uk/living-standards-poverty-and-inequality-uk.

Source:

Institute for Fiscal Studies. Living standards, poverty and inequality in the UK. Available at: https://ifs.org.uk/living-standards-poverty-and-inequality-uk.

Source:

Office for National Statistics. Labour Market Statistics: Current Dataset. Office for National Statistics, 2025. Available at: https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/datasets/labourmarketstatistics/current.

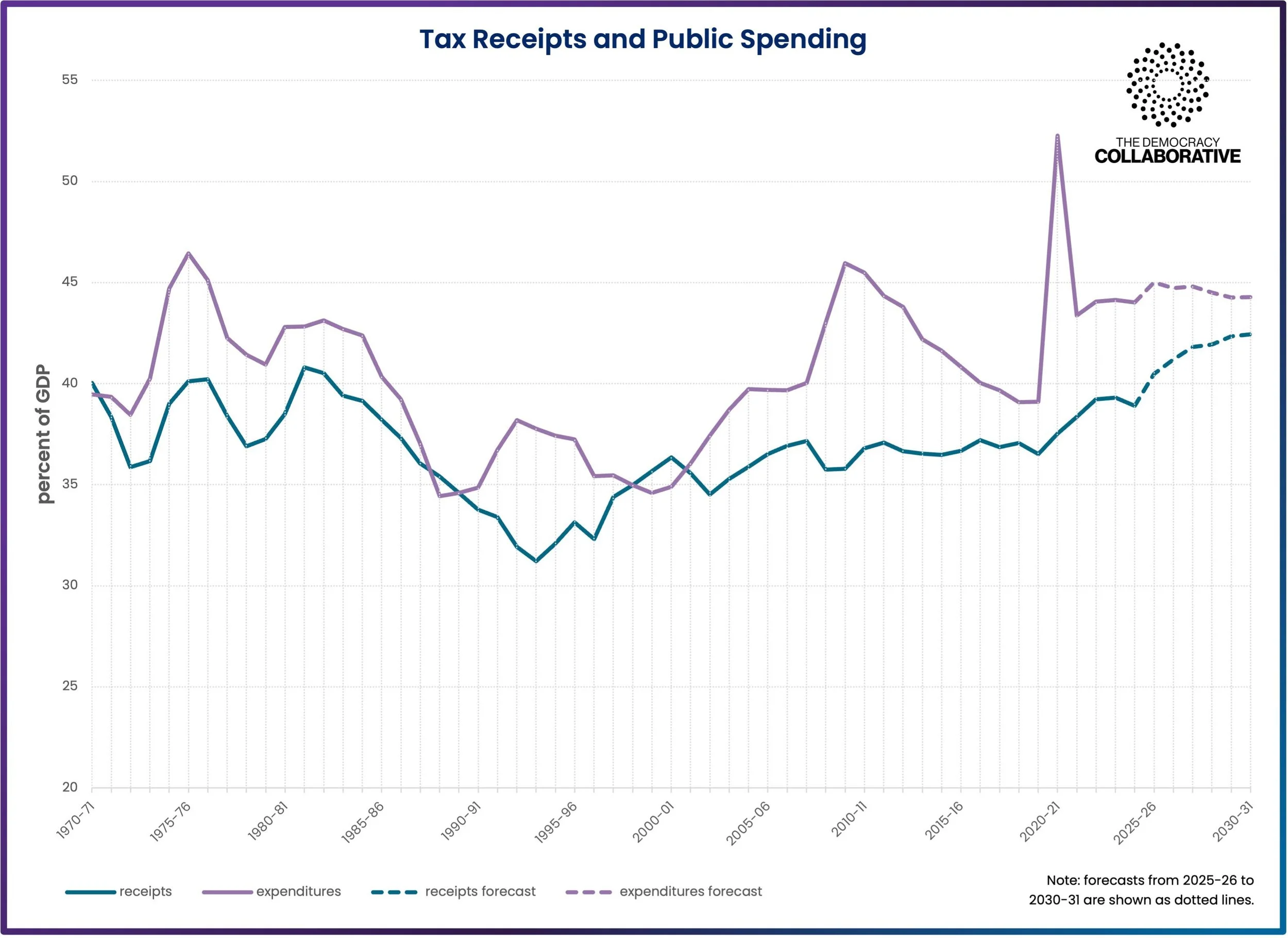

Like growth, public debt is often taken as a significant barometer of national economic health in Britain – especially by international institutions and investors. It also guides economic and social decision-making, and the current Labour government has committed to a series of fiscal “rules,” including a lowering of public debt.[25]

“We should be cautious in adopting public debt as a true indicator of economic health. In our view, public spending and public debt are not inherently problematic.”

We should be cautious in adopting public debt as a true indicator of economic health.

In our view, public spending and public debt are not inherently problematic – although this is fiercely contested across the political spectrum, and is certainly not the view that pertains at the centre of the present economic orthodoxy in HM Treasury and the City of London.

Other considerations are often conflated with the issue of public debt, such as the effects of the tax burden and of whether there is value for money in public services.

There is a genuine political issue around the question of the – accurate – perception that Britons are not recipients of the benefits of high-quality public services commensurate with their present tax burden – a political struggle that goes back to the origins of the modern state and accompanying efforts to limit the tax-raising powers of absolutist monarchs by merchant classes via fiscally sovereign parliaments. This was the context in which the Bank of England was originally created under William III in 1694, and there has been a continuous public debt in the modern sense ever since.[26]

Public debt, as Barry Eichengreen and his co-authors point out in their book In Defense of Public Debt, has historically had vitally important uses, including the ability of governments to finance emergency responses to wars and pandemics or to lay the foundations of essential public goods and services such as health, education, and transport.[27]

But there is also the matter of the servicing of that debt. In a low-growth environment such as Britain has experienced for the last several decades, debt repayments are understood as constraining other spending and investment not just politically (i.e. the fiscal rules) but also economically.

As a feature of current institutional arrangements, and in the absence of widespread public comprehension of the existence of alternative monetary arrangements such as direct monetary financing, the public debt is widely perceived to be an insupportable burden.

Alternative approaches to macroeconomic management are precluded politically by the persistence of orthodox economic doctrine and media recourse to the “household analogy” in public finances – the mistaken belief that taxes “pay for” public spending, and that “the books must balance” for the economy as a whole as for any given household or business within it. [28]

In fact, it has been clearly established in a step-by-step walk-through of everyday UK monetary operations that the government first spends into the economy and only later taxes back or issues debt: “public expenditure is always financed through money creation rather than taxation or debt issuance.”[29]

That said, we are unlikely to see a revolution in public understanding of macroeconomic management in the near term, and therefore the public debt currently operates as a continuing political constraint on UK economic policy options, including social spending.

Currently, Britain is projected to spend £111.2 billion in interest payments on its public debt in 2025-26 (8.3% of total public spending and over 3.7% of GDP).[30]

Public sector net debt (as a percentage of GDP) fell dramatically in the postwar period, and stood at 54.7% in 1970-71. It subsequently fell even lower, hitting 21.6% in 1990-91, before increasing dramatically in the past two decades to its current level of around 94%. This increase has been fueled by a combination of increased borrowing, low growth, and – more recently – the return of high interest rates in the period since the COVID-19 pandemic and Ukraine War energy price shock.

Although UK national debt has been much higher (as a share of national product) in earlier periods, such as the Napoleonic Wars and the periods following the two World Wars, at present levels it is high by peacetime historical standards.

Chart 10: Public Debt

Source:

Office for Budget Responsibility. Public finances databank 2025–26. Published 21 August 2025. Available at: https://obr.uk/public-finances-databank-2025-26/.

Source:

Office for Budget Responsibility. Public finances databank 2025–26. Published 21 August 2025. Available at: https://obr.uk/public-finances-databank-2025-26/.

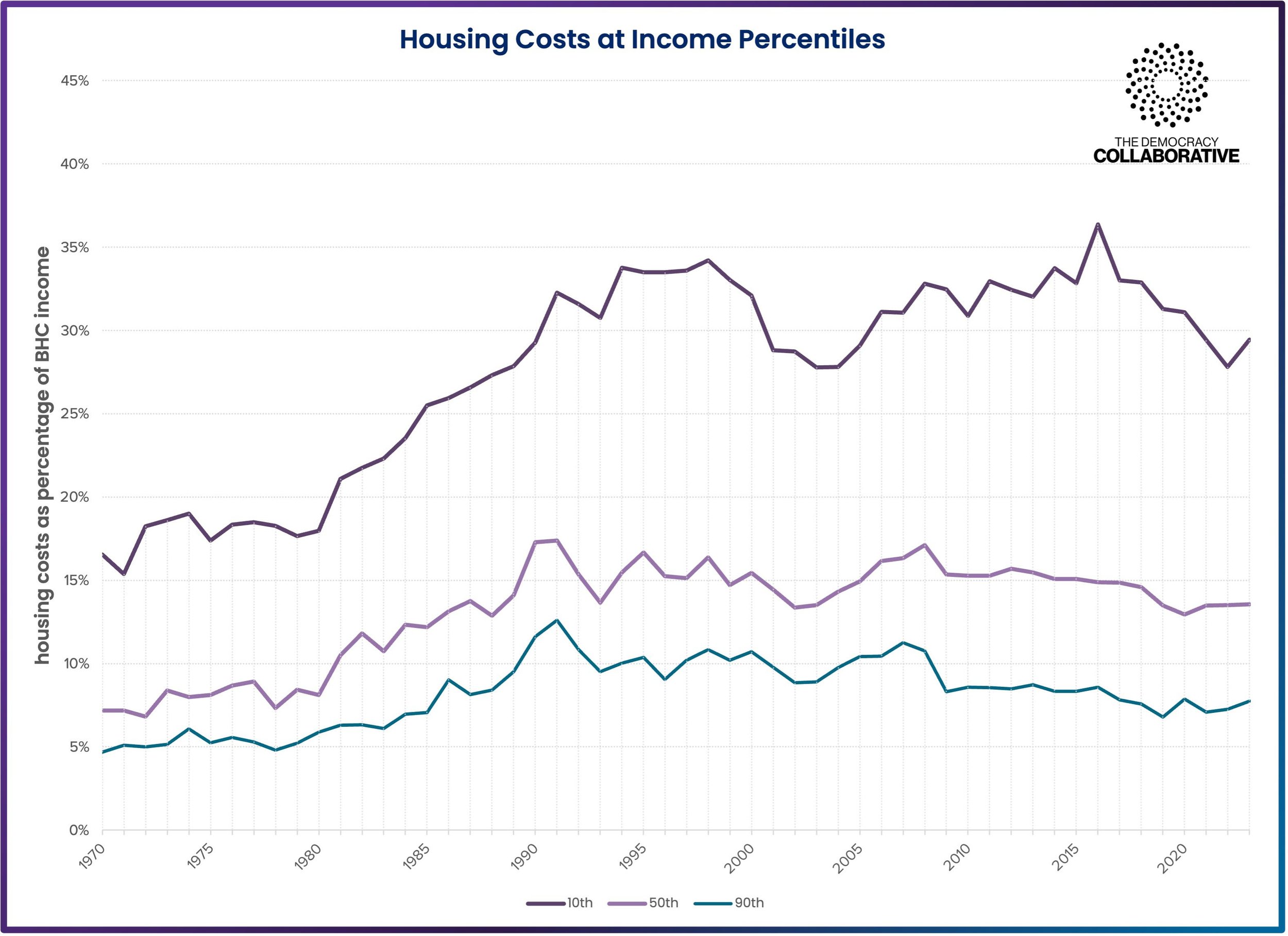

“A major component of the present cost-of-living crisis is also a steady increase in the cost of housing over the past 50 years.”

As will be further discussed in Appendix A below, Britain is often described as being in the midst of a severe “cost-of-living crisis.”[31] While this is at least partially attributable to recent increases in product and commodity inflation, a major component of the present cost-of-living crisis is also a steady increase in the cost of housing over the past 50 years.

Housing is a major element in the story of Britain’s descent into systemic crisis.

As the Common Sense Policy Group argue in their recent manifesto Act Now: A Vision for a Better Future and a New Social Contract, the housing sector in Britain features “gross regional inequalities in housing costs, falling levels of ownership and high levels of homelessness,” and that this is at least in part due to an extractive and financialised house-building industry “failing to meet the need for sustainability and affordability.”[32]

“Sooner or later,” as Josh Ryan-Collins, Toby Lloyd, and Laurie Macfarlane warn in their book Rethinking the Economics of Land and Housing, “either a crash in property values will reset the market or housing market failure will weigh down ever more heavily on the economy, until the growing frustration of those paying ever larger proportions of their wages in rents triggers a political crisis, with unpredictable consequences.”[33]

The rise in unaffordability of housing is clear in the time series data.

In 1970, social renters paid around 8.7% of their income on housing; private renters paid around 9.4%; and homeowners paid around 5.9%. These percentages slowly climbed through the 1970s before exploding in the 1980s and early 1990s and then somewhat stabilizing at higher levels. In 2023, social renters paid around 23.6% of their income on housing (a 171.2% rise since 1970); private renters paid around 28.1% (a 198.9% rise); and homeowners paid around 9.9% (a 67.8% rise).

In housing, as with the economy as a whole, these patterns are unlikely to shift significantly without major structural change in the housing market – in this instance through interventions capable of “wrest[ing] our cities back from the hands of the rentier, landlord and speculator.”[34]

Chart 12: Housing Costs

Source:

UK Data Service. Family Expenditure Survey (1961–1993) and Family Resources Survey (1994/95–2023/24). Analysis by Howard Reed

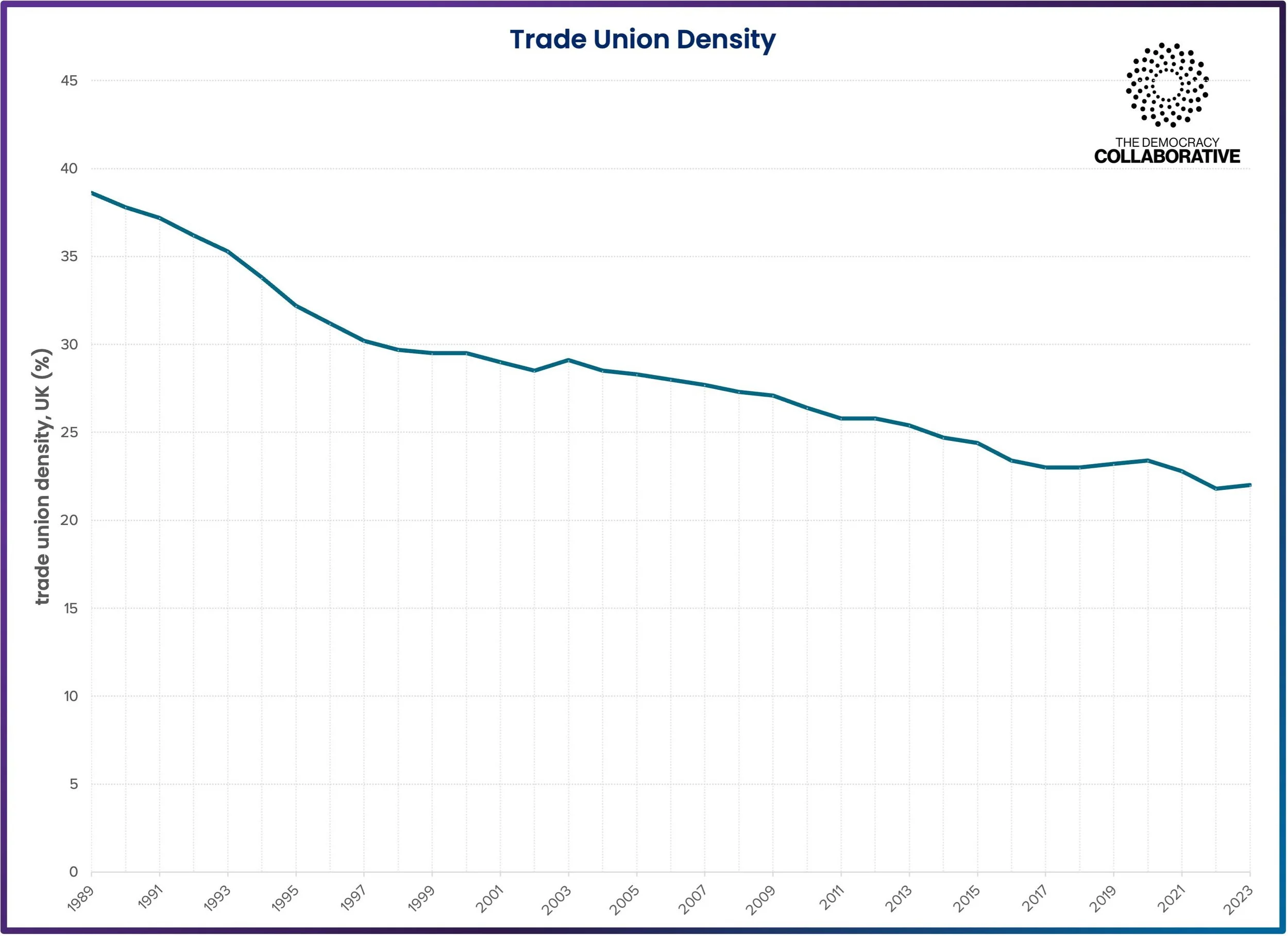

Research shows that union membership is associated with higher wages and reduced income, racial, and gender inequality.[35]

Trade unions are a principal means by which labour exercises its bargaining power with capital owners, and stronger unions are better positioned to extract greater compensation and other concessions from employers.

Higher trade union density also has a demonstrably positive effect on a range of social and civic outcomes, which can be transmitted through political and policy and even cultural as well as through economic and employment channels.[36]

Conversely, falling trade union density means weaker bargaining power, and therefore corresponds to deteriorating wages and conditions. The reduction in the power of the “countervailing force” that trade unions allow labour to exert in a system otherwise dominated by capital is likely one of the core explanations for the deteriorating conditions affecting a majority of Britons in recent decades.

In Britain, union membership reached a peak of around 13 million workers in the late 1970s. In subsequent decades, union membership rapidly declined, hitting a current low of around 6.1 million workers in 2024. As a percentage of the labor force, union membership has fallen from 38.6% in 1989 (the first year comparable records are available) to just 21.5% in 2024, a reduction of 17.1 percentage points.

Chart 13: Union Membership

Source:

Department for Business and Trade. Trade union statistics 2024. Published 22 May 2025. Available at: https://www.gov.uk/government/statistics/trade-union-statistics-2024.

Source:

Department for Business and Trade. Trade union statistics 2024. Published 22 May 2025. Available at: https://www.gov.uk/government/statistics/trade-union-statistics-2024.

Long-term underinvestment is a chronic feature of Britain’s ailing economy, deteriorating outcomes, and poor prospective outlook.

The high growth rates of the postwar period in Britain were at least in part driven by sustained public investment in the economy, housing, and public and social services. In the 1950s and 1960s, gross public investment was never less than around 7% of GDP, peaking at 11.4% in 1967/68. After 1975/76, gross public investment declined rapidly, reaching 2.7% of GDP in 1996/97. There was a limited recovery in the 2000s, but gross investment has not passed the 6% mark since the mid-1980s. In 2024-25, gross public investment stood at just 4.9%.

Private sector investment has not made up for this decline.

Overall, total public and private sector investment in Britain (measured by Gross Fixed Capital Formation) has declined since the 1970s. After hitting a peak of 26.4% of GDP in 1976, it subsequently fell and then rebounded during the 1980s, before dropping precipitously in the 1990s and then stabilizing. In 2024, total public and private investment amounted to around 17.4% of GDP, a 34.1% decline from 1976.

Chart 15: Investment

Source:

Office for Budget Responsibility. Public finances databank 2025–26. Published 21 August 2025. Available at: https://obr.uk/public-finances-databank-2025-26/.

Many of Britain’s economic challenges, including around investment, are at least partially connected to the international exposure of the UK economy through globalization and “free trade” – both of which are prominent features of the neoliberal economic model installed at home and abroad in the 1980s and 1990s.

As the birthplace of industrialisation, Britain had a first-mover advantage, and “free trade” has often been described as akin to the national religion, typified by the outlook of The Economist magazine and dating back to the Enlightenment thinking of classical economists such as Adam Smith and David Ricardo.

Whilst there is great debate about both the extent and effects of globalisation and free trade on the British economy, it is increasingly accepted that these have not been as universally positive as their supporters often contend.

The UK is usually considered to be relatively successful in attracting foreign direct investment (FDI), often appearing in the top twenty largest recipients of inward FDI globally. A lot of this, however, has not been greenfield investment but Merger & Acquisition activity (the vast majority) and intra-company loans, the latter including activity related to transfer pricing and other tax shenanigans, rather than bona fide productive investment.

Moreover, the UK has consistently become a net outward investor overall.

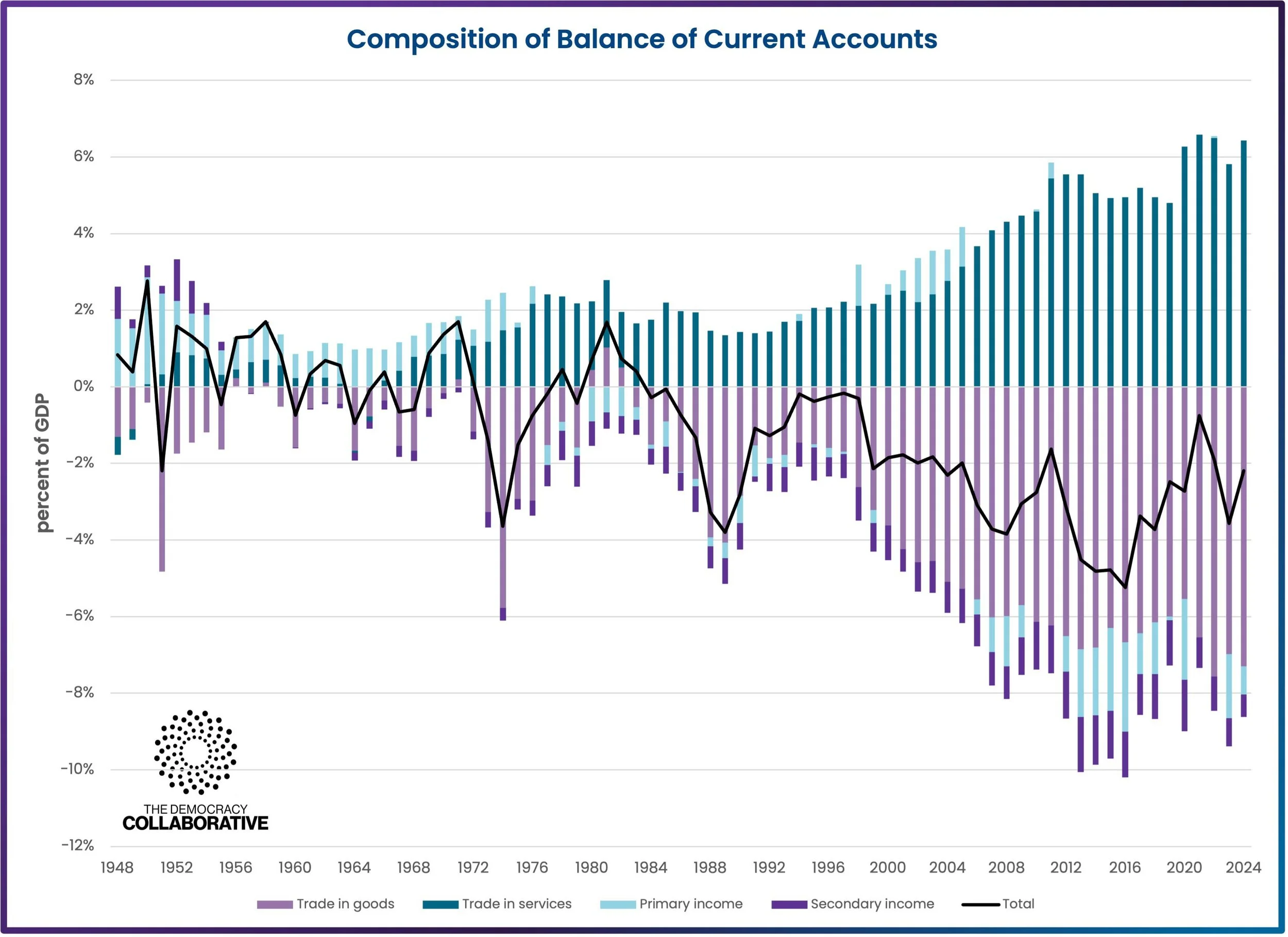

One key indicator is the imbalance of financial flows that amount to growing financial extraction by overseas owners of the British economy, which is itself connected to the country’s balance of trade with the rest of the world.

In the 1950s and 60s, Gross National Income (GNI) was generally greater than Gross Domestic Product (GDP), meaning that income was flowing into the country from overseas. However, in the mid-1970s this direction reversed and the volume of financial outflows has been volatile, but growing, ever since. In other words, an increasing amount of income is flowing out of Britain, rather than into it.

This corresponds with Britain’s trade balance, which has been mostly negative (more imports than exports) since the mid-1980s. Overall, Britain’s balance of payments for goods and services has been in deficit since 1984. Prior to that, it fluctuated but was often positive. Between 1946 and 1983, the average balance was 0.3% of GDP. From 1984 to 2024, the average balance was -2.2%.

Chart 16: Financial Extraction

Source:

Office for National Statistics. United Kingdom National Accounts: The Blue Book 2024. Published 31 October 2024. Available at: https://www.ons.gov.uk/economy/grossdomesticproductgdp/compendium/unitedkingdomnationalaccountsthebluebook/2024.

Source:

Office for National Statistics. United Kingdom Balance of Payments: The Pink Book 2024. Published 31 October 2024. Available at: https://www.ons.gov.uk/economy/nationalaccounts/balanceofpayments/bulletins/unitedkingdombalanceofpaymentsthepinkbook/2024.

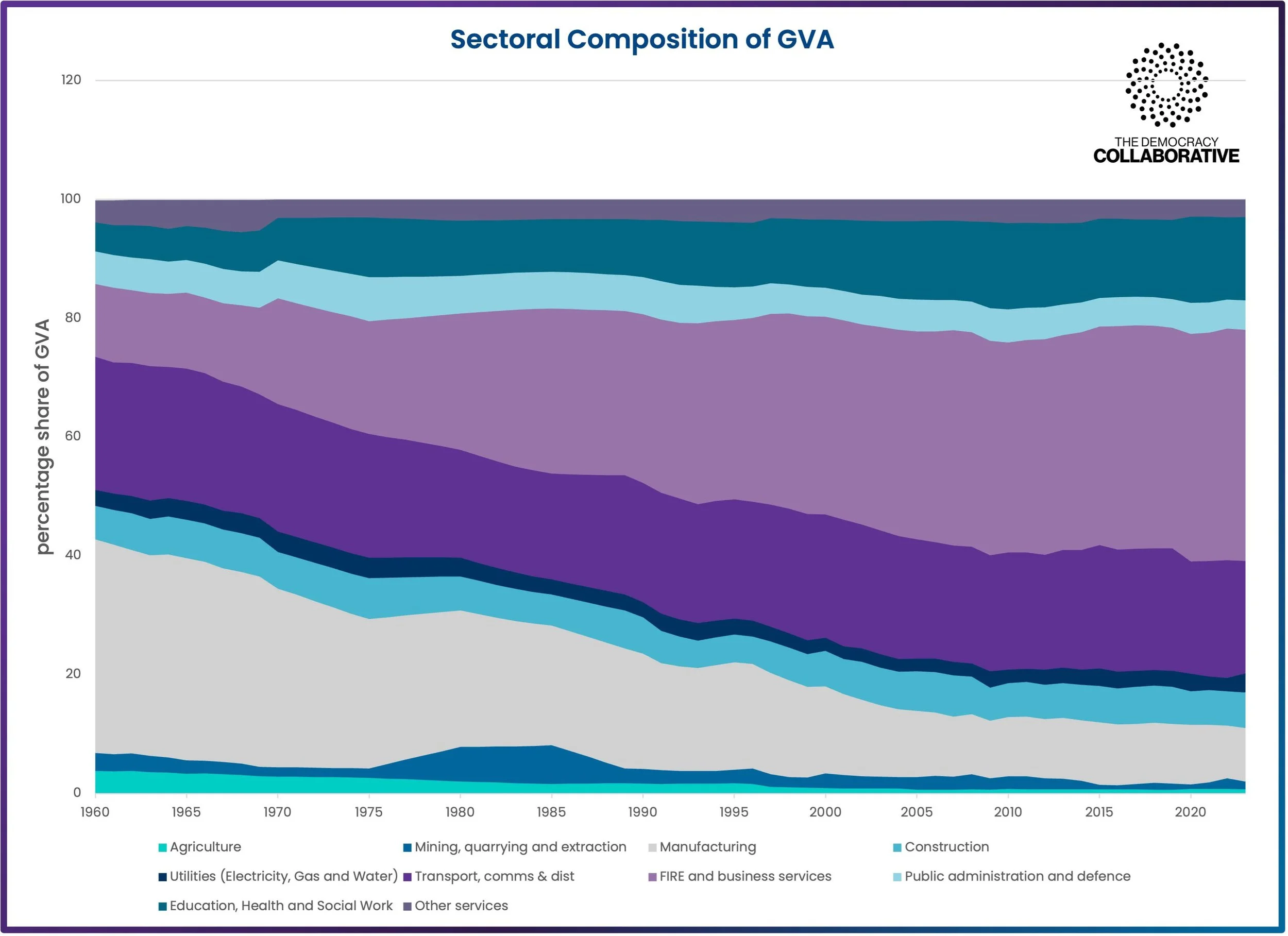

The reversal of Britain’s trade balance reflects a larger shift in its economic orientation from manufacturing to services – and, in particular, financial services.

In 1960, manufacturing accounted for 36% of Gross Value Added (GVA), with total production and construction accounting for 47.3%; Services accounted for 48.8%, with the FIRE sector (finance, insurance and real estate) accounting for 12.2%.

Since then, the British economy has basically flipped. In 2022, manufacturing was just 8.8% of GVA (down 27.2 percentage points from 1960), with total production and construction accounting for 18.7% (down 28.6 percentage points). Services accounted for fully 80.6% (up 31.8 percentage points), with the FIRE sector accounting for 39% (up 26.8 percentage points).

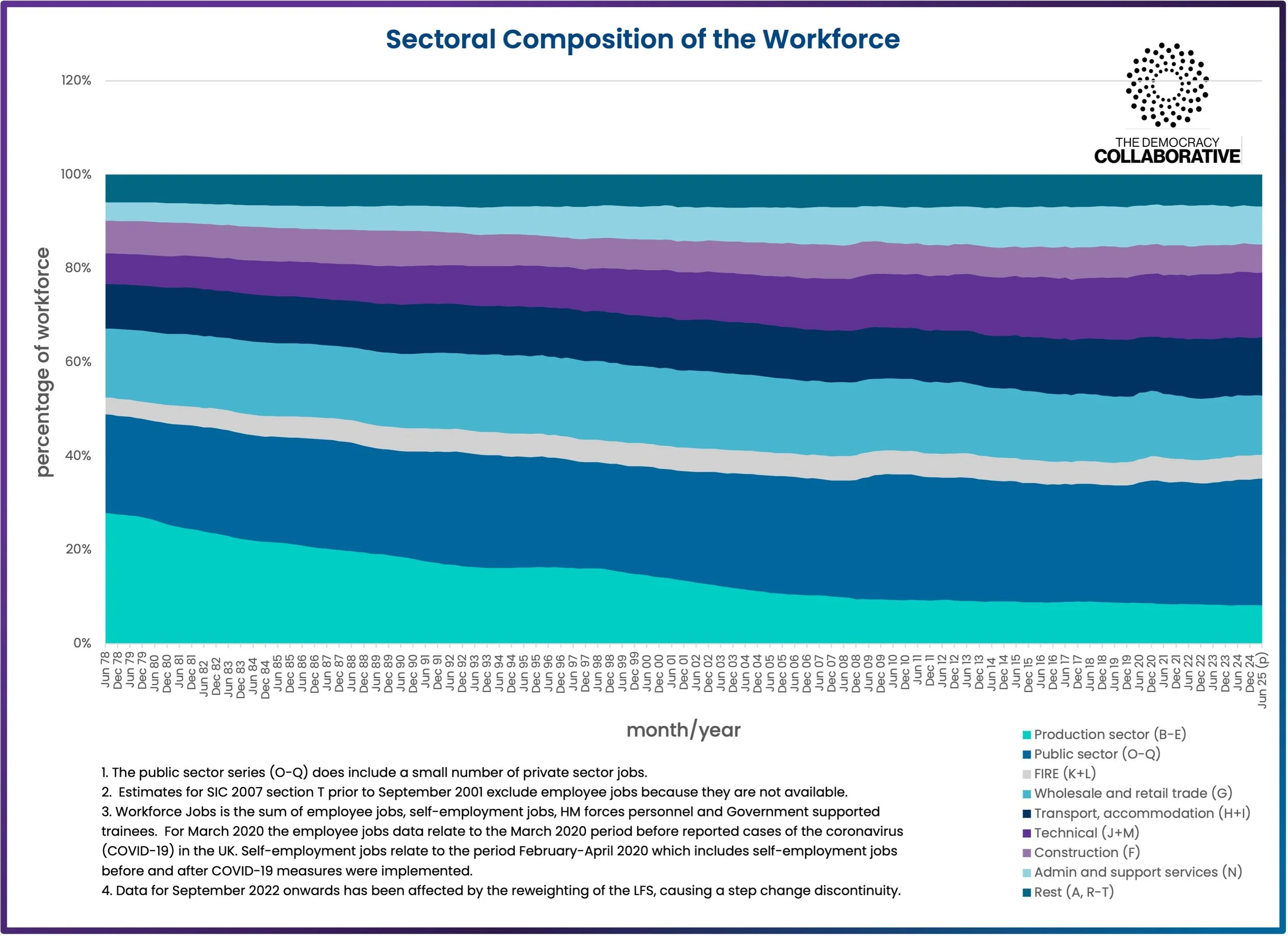

Importantly, the growth of the FIRE sector in terms of GVA has not been matched with a corresponding growth in employment. In 1978, the FIRE sector accounted for just under 4% of the workforce. By 2025 this had barely grown to 5.1%. By contrast, production sector employment fell dramatically from 28% to just 8%.

In other words, as will be discussed further in section 2 of this Index, the seismic shifts in the orientation of the British economy over the past several decades have primarily benefited capital rather than labour.

Since 1995, growth in the value of financial assets and real estate has far outpaced both GDP and weekly earnings, indicating continued decoupling of the “productive” and “speculative” economies.

“Far from boosting productivity and increasing efficiency in the non-financial economy, the growth of the financial sector functions as a subtraction from the real economy, as financial flows are diverted to unproductive uses and the resulting revenue flows benefit a minority.”

There is a growing gap between the headline performance of the economy as seen in the London Stock Exchange and what more and more people report as their own economic position and the financial stresses and worries which they carry.

The vast wealth of the UK economy is not being experienced as such by most people. GDP may increase, the stock market may rise, but for many there is only the growing squeeze on incomes and the accumulating debt burden.

Part of the explanation for this gap is the hidden economic process of financialisation, by which financial flows are diverted away from production and consumption toward asset markets in the pursuit of capital gains.

Financialisation is not yet widely enough understood, even as it becomes the increasingly damaging force behind the extractive economy and its consequences for workers, society, and the natural world.

Financialisation is a complex phenomenon, but has enormous explanatory power as to the causes of Britain’s highly unequal and dysfunctional economy of growing poverty in the midst of plenty.

Far from boosting productivity and increasing efficiency in the non-financial economy, the growth of the financial sector functions as a subtraction from the real economy, as financial flows are diverted to unproductive uses and the resulting revenue flows benefit a minority.

As financialisation gathers pace, rising wealth and debt detract from income for the majority.[37] In such an economy, what is counted as growth matters a great deal. Every financial asset is at one and the same time someone else’s financial liability – and as the holdings of the financial sector have increased, so too has the debt held by households and businesses in the non-financial economy.

This dynamic goes by the name of assetisation, which is “the creation of assets and liabilities out of future economic activity.”

As Dirk Bezemer, Michael Hudson and Howard Reed describe assetisation in a paper produced for The Democracy Collaborative:

“Students’ future incomes are capitalised into student loans, households’ into mortgages. Future mobility is capitalised into car loans, future pensions into pension assets, future profits into equity. Each of these assets is held as a liability by the issuer, who must service it out of their incomes, both wages and profit, by paying interest, dividends, contributions to pensions and social security. This extraction constitutes ‘savings’ in the sense of non-consumed income. But… these ‘savings’ are not necessarily supporting production. They are payments for debts and to gain access to utilities, education, infrastructure and other necessities that have been turned into assets requiring a return. Basic necessities are redefined as assets, whose price is inflated by the liquidity poured into asset markets. This is the new ‘circular flow’ logic of the capital gains economy.”[38]

The result, our economists point out, is “lower disposable incomes, even before taxes. For instance, rents increase when house prices rise. Water utilities are turned into privately traded assets; then the fees are increased to pay for the increased asset costs. Firms are acquired on debt; then disposable wages fall, after servicing the new debt liabilities. As income growth declines to generate capital gains to asset owners, this adds to the attractions of holding assets. Increasingly, income inequality comes to be defined by the dichotomy between the haves in asset markets, who reap capital income and capital gains, and the have nots, who service the liabilities that make capital income and capital gains possible.” [39]

This process of financialisation in pursuit of capital gains helps explain the squeeze-play of recent years, whereby nominal economic growth has in reality been experienced as reduced income through increased extraction and indebtedness.

The data show the powerful development of financialisation in the UK.

Between 1995 and 2020, nominal wages doubled, nominal UK GDP rose two and a half times, while average house prices quintupled and the valuation of financial assets rose four and a half times.

The benefits of Britain’s “capital gains economy” are revealed as flowing primarily to asset-owners and the already wealthy, while for the rest of us there are lower earnings from work, lower income growth in the non-financial sector, lower productivity, and less innovation – all alongside sizable increases in debt and (conversely – as every debtor has a creditor) in financial and real estate wealth.

The financial sector is extractive from the real economy.

Given that all income groups are paying ever more into the finance sector in fees and interest charges and for underlying assets while the payouts from the sector are even more concentrated than those of the economy as a whole, the finance sector has also become the locus of the production of increased inequality in the UK economy.

Chart 18: Manufacturing and Services (GVA Share)

Source:

Bank of England. A Millennium of Macroeconomic Data for the UK. Version 3.1, updated to 2016. Available at: https://www.bankofengland.co.uk/-/media/boe/files/statistics/research-datasets/a-millennium-of-macroeconomic-data-for-the-uk.xlsx

Office for National Statistics. United Kingdom National Accounts: The Blue Book 2024. Published 31 October 2024. Available at: https://www.ons.gov.uk/economy/grossdomesticproductgdp/compendium/unitedkingdomnationalaccountsthebluebook/2024.

Source:

Bank of England. A Millennium of Macroeconomic Data for the UK. Version 3.1, updated to 2016. Available at: https://www.bankofengland.co.uk/-/media/boe/files/statistics/research-datasets/a-millennium-of-macroeconomic-data-for-the-uk.xlsx

Office for National Statistics. United Kingdom National Accounts: The Blue Book 2024. Published 31 October 2024. Available at: https://www.ons.gov.uk/economy/grossdomesticproductgdp/compendium/unitedkingdomnationalaccountsthebluebook/2024.

Source:

Office for National Statistics. JOBS02: Workforce jobs by industry, 16 December 2025.

Available at: https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/datasets/workforcejobsbyindustryjobs02.

Chart 21: Financialisation Overview (Since 1995)

Source:

Office for National Statistics. Earnings time series of median gross weekly earnings from 1968 to 2022. Published 2025. 2025. https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/earningsandworkinghours/datasets/earningstimeseriesofmediangrossweeklyearningsfrom1968to2022; Office for Budget Responsibility. Public finances databank 2025–26. Published 2025. https://obr.uk/public-finances-databank-2025-26/; HM Land Registry. UK House Price Index (Browse Tool). Available at: https://landregistry.data.gov.uk/app/ukhpi/browse.

The longevity of the neoliberal economic model over the past several decades, as well as continued support for it, can be partially explained by the existence of a veneer of prosperity that obscures some of the weaker or deteriorating underlying trends.

In other words, the model often works for a small subset of the population who are able to grow their wealth and power. Then, through cultural and political reinforcement, these examples are offered as “proof” that the economy is delivering positive economic results.

However, investigating trends in inequality over time exposes this myth and demonstrates that the British economy is increasingly working only for an increasingly small fraction of the population. As financial extraction grows and the capital gains economy becomes the basis of accumulation, the squeeze on wages and living standards intensifies. Politicians insist that not much can be done about this in the short term because – in the constant refrain of austerity economics on both front benches – “the money isn’t there.”[40]

This is a political fiction.

The United Kingdom is the sixth largest economy in the world. By any measure, it is one of the richest societies in human history. But nowhere does it appear this way except in the precincts of the very wealthiest, for whom the system is delivering vast material gains and great financial prosperity.

“Despite the dire state of the country, the problem is not a shortage of resources, but rather that plentiful resources are hoarded at the top.”

That Britain does not feel affluent is a result of the extremes of growing inequality and the diversion of wealth and productive capacity away from public goods and services to elite private accumulation and consumption. The story is one of concentrated private affluence amidst widespread and growing public squalor.

Despite the dire state of the country, the problem is not a shortage of resources, but rather that plentiful resources are hoarded at the top.

By way of comparison, in 1945 the postwar Labour government inherited a war-shattered economy laden with debt and had to literally rebuild amidst the ruins. But they managed to create the NHS, nationalised a fifth of the economy, and established the welfare state and the postwar settlement – a truly transformative programme that reshaped the political economy for decades to come.[41] In real terms, Britain’s GDP in 1945 was £383 billion, compared to around £2.3 trillion today; we are more than five times richer in real terms than Attlee’s Britain.

But it’s even better than that. Britain today is not only richer than Attlee’s Britain, but is also richer in real terms than Harry Truman’s United States – the colossus that bestrode the globe and helped reconstruct war-torn Europe and Japan through the Marshall Plan. America’s GDP in 1945 was equivalent to £1.95 trillion today.

The story that Britain lacks the resources to tackle child poverty or to invest in public services or to drive the green transition or rebuild the depleted public realm is exactly that – a story. There is greater wealth in Britain today than was available to the U.S. superpower constructing the postwar international order.

There is just a political unwillingness to shift the resources of a rich system from private accumulation to public need.

Historically, Britain had high levels of income and wealth inequality due at least in part to the existence of a monarchy and landed aristocracy and the continual passing down of inherited fortunes.

From around 1914 onwards, income inequality began to fall – a process accelerated by the Depression era, the Second World War, and the post-war social democratic period which saw the construction of the modern welfare state. In 1978, income inequality hit its lowest point before rising considerably in the 1980s. Since then, there have been further (uneven) increases in income inequality. In 2023, the Gini coefficient (after housing costs) was 0.387, up more than 56% from 1978.

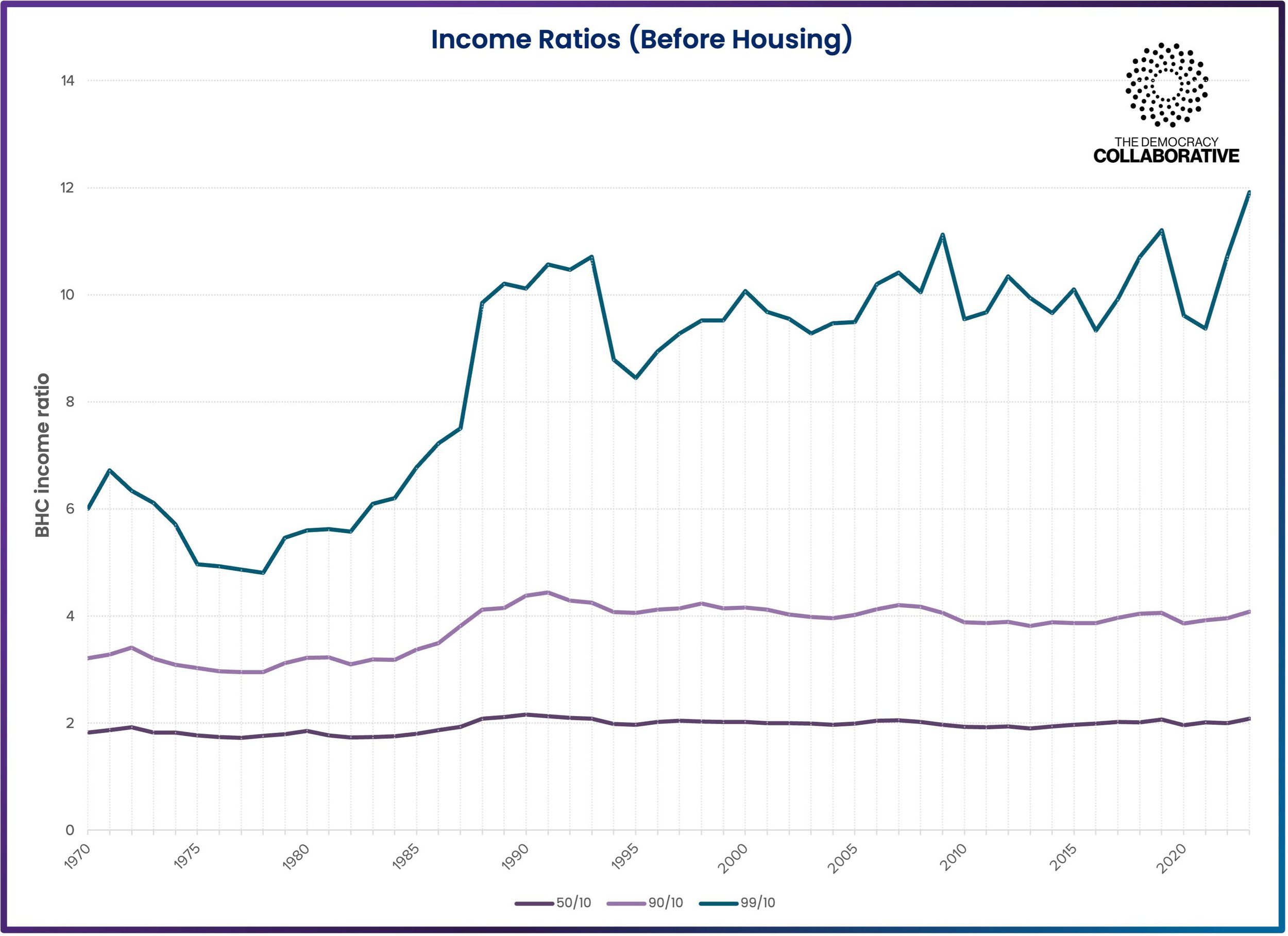

Furthermore, the rise in income inequality since the 1980s has been driven mostly by the top 1% of earners. In 1978, the ratio of the 99th percentile (top 1% of earners) of net income (after housing) to the 10th percentile (bottom 10% of earners) was 5.6; by 2023 it had risen to 15.56 (a 177.8% increase). By comparison, for the 90th percentile (top 10% of earners) the rise was 71.7%; and for the 50th percentile (top 50% of earners) the rise was 42.4%.

Chart 22: Income Inequality

Source:

Institute for Fiscal Studies. Living standards, poverty and inequality in the UK. Available at: https://ifs.org.uk/living-standards-poverty-and-inequality-uk.

Source:

Institute for Fiscal Studies. Living standards, poverty and inequality in the UK. Available at: https://ifs.org.uk/living-standards-poverty-and-inequality-uk.

Source:

Institute for Fiscal Studies. Living standards, poverty and inequality in the UK. Available at: https://ifs.org.uk/living-standards-poverty-and-inequality-uk.

Source: